Few people manage to save half of their income. But those who do, and stick with it over, are sure to be rewarded for it in the end. But just how good is it? How much better is it to save 50% rather than the average savings rate?

Here’s the short answer:

Yes, saving 50% of your income is good. It’s ten times better than the average personal savings rate. Given a median income, you can become a millionaire in 19 years if you invest it all in index funds.

But you’re probably not looking for “the short answer”…

The focus of this article will be to figure out where you will end up by saving 50% of your income. I’ll also give you some guidelines as to how you can achieve a personal savings rate of 50%.

But first, I’ll look closer at how much better 50% is than the average savings rate.

Saving 50% Of Your Income vs The Average:

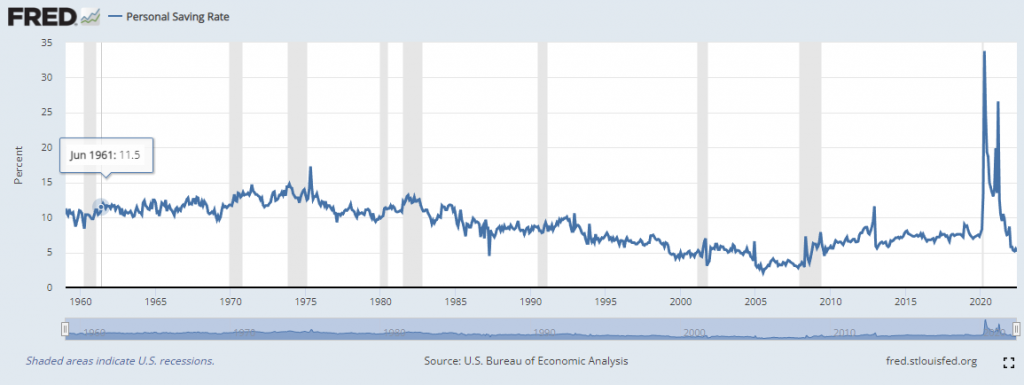

On average, Americans save only 5 percent of their income. That’s based on data from The U.S. Bureau of Economic Analysis. (source)

You don’t need a master’s degree in mathematics to see that saving 50% is WAY better than the personal savings rate has ever been…

Let’s assume you’re earning a median income of roughly $56,000 annually.

With a personal savings rate of 5%, you’d save $2,800 annually.

With a personal savings rate of 50%, you’d save $28,000 annually.

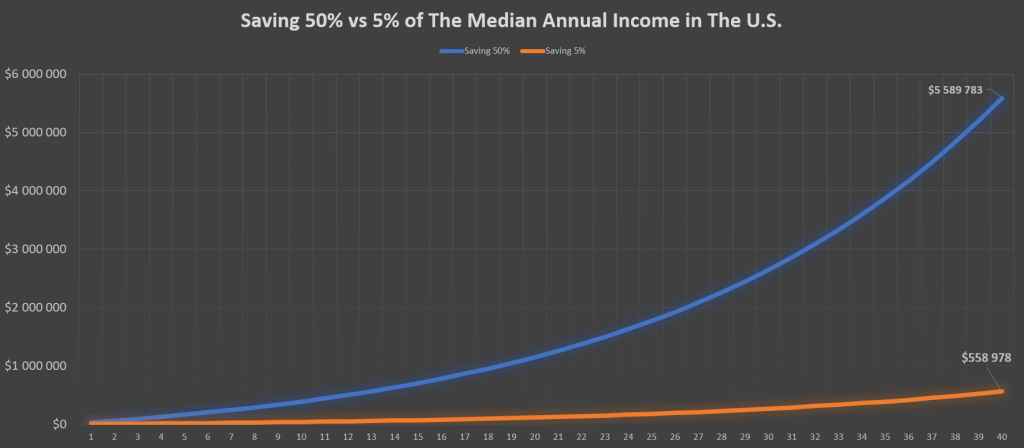

What if you invest it? After all, saving money won’t make you rich; you should put those bills to work! I’ll use saving and investing synonymously in the rest of the article. On the chart below you see how much more you’ll have over a 40-year period if you save 50% annualy rather than the average of 5%:

Saving 50% of the median income for 40 years nets you roughly $5.5 million, while 5% barely gets you above haf a million.

After 19 years, saving 50% of the median annual income turns into one million dollars.

Enough comparison to the average and median. Let’s look closer at your specific situation.

Suggested reading: How Much Should YOU Save Per Year?

Will Saving Half Your Income Make You Wealthy?

Let’s define wealthy as having $1,000,000 saved up. The question then becomes how much do you need to earn annually for a personal savings rate of 50% to be sufficient to become wealthy?

I’ve made a bunch of different examples in a few tables you can see below. Try to find your annual income and see how long you need to save 50% of it to become wealthy:

| Annual Income | Annual Savings (50%) (Invested at 7% returns) | Years To Wealth ($1,000,000) |

|---|---|---|

| $20,000 | $10,000 | 31 |

| $25,000 | $12,500 | 28 |

| $30,000 | $15,000 | 26 |

| $35,000 | $17,500 | 24 |

| $40,000 | $20,000 | 23 |

| $45,000 | $22,500 | 21 |

| $50,000 | $25,000 | 20 |

| $55,000 | $27,500 | 19 |

| $60,000 | $30,000 | 18 |

| $65,000 | $32,500 | 17 |

| $70,000 | $35,000 | 17 |

| $75,000 | $37,500 | 16 |

| $80,000 | $40,000 | 15 |

| $85,000 | $42,500 | 15 |

| $90,000 | $45,000 | 14 |

| $100,000 | $50,000 | 13 |

| $125,000 | $62,500 | 12 |

| $150,000 | $75,000 | 10 |

It is interesting to see that saving 50% of $50,000 only takes twice as long to reach a million as saving 50% of $150,000.

One might think that saving three times as much would shorten the time needed to reach a million by two thirds, but that’s wrong due to the power of compound interest.

Anyways, I hope you found your personal annual income in the table above, or at least something close to it!

How To Save Half Your Annual Income

Saving half of your income is no easy feat. It’ll take dispiplin and careful planning of expenses. Nevertheless, it’s highly rewarding, and allows you to sleep better than most people; the median balance for checking and savings combined is a modest $5,300. (source)

In this section, I’ll give you the most valuable insight I’ve gained over my years of researching and learning about personal finance. However, to get a complete guide on saving more money, check out this article instead: The 4 Steps To Save A Lot Of Money Fast

Do this to save half of your income:

Understanding this principle is key:

Small things make a small impact. Big things make a big impact.

Most people think that “luxuries” like Netflix and Starbucks are what keep them unable to save more money, but that is wrong.

Your main focus should NOT be on small, variable expenses like Netflix and Starbucks. Focus on the big, fixed expenses like housing and transportation.

This is essential for two reasons:

You save big money by cutting down on big stuff, and by focusing on fixed expenses you’ll save that money consistently.

To reach your goal, here’s what you must do:

- Cut down on housing expenses. Housing is by far the biggest expense for most people. If you can cut down on this one, you’ll be able to save a lot more money every month. For example, if you spend $20,000 per month on housing, but you’re able to cut that down by 40%, you’ve already got $8,000 per month!

- Cut down on commute-related expenses. This is often the second largest expense people have. If you can cut this one down, you’re left with a big chunk of money to save every year.

- Shop for insurance and utilities. Insurance and utilities stack up fast. Once every year you should go through it all and “shop around” for better alternatives. Big bucks can be saved on this.

The #1 move to save a lot of money:

If you love your finances, you should do the following:

Move closer to work, in a cheaper house/apartment.

This move cuts down on your housing expenses and transportation costs in one go. It’s likely that you’re saving on utilities as well.

In fact, if you’re able to move close enough, you might consider biking or walking to work, almost eliminating your transportation costs entirely.

This is by far the most powerful financial move you can make.

If you need more on saving more money, check out this article: Can’t Save Money Because of Bills? Here’s What I Did

To summarize:

Cutting down on big fixed expenses like housing and transportation is the best way to save 50% of your expenses.

In addition, the saving will be consistent because you cut down on “fixed” expenses.

If you think 50% is too much, you can read one of these articles instead:

- Is Saving 20% Of Your Income Enough?

- Is Saving 25 Percent Of Your Income Good?

- Is Saving 30 Percent Of Your Income Good?

- Is Saving 40% Of Your Income Good?

Conclusion: Yes, Saving 50% Of Your Income Is Good

Saving half your income is ten times better than the average savings rate of 5%. Given a median income, saving 50% of it will turn into a million in 19 years. After 40 years, it’ll be $5.5 million.

The best way to reach a savings rate of 50% is to focus on big “fixed” expenses like housing and transportation. Moving closer to work is the most effective action you can take.

Thank you for reading!

– Oskar