We’re all trying to save more money. But how much is enough? I see the classic “save 20% of your income” all over the place, but is that enough?

Yes, saving 20% of your income is enough for most people. It’ll ensure a good retirement and sufficient short-term savings for things like trips, a new car, or unexpected significant expenses.

But you don’t care about “most people”. You want to know if saving 20% of your income is enough for you!

In this article, I’ll help you figure out just that. I’ll show you a simple four-step process that’ll answer your question.

If you find saving 20% of your income easy and want a real challenge, check out one of the other articles I just wrote:

Is Saving 25% Of Your Income Good?

Is Saving 30% Of Your Income Good?

Is Saving 40% Of Your Income Good?

Is Saving 50% Of Your Income Good?

Warning: I’m a “math guy”. You’ll have to forgive me if I throw a bunch of charts and tables as you…

Is Saving 20% Of Your Income Enough?

First off, saving 20% of your income is great. If you’re doing that, you’re a financial outlier.

In my article about how much money you should save every year, you’ll see that it’s likely close to 20% of your income.

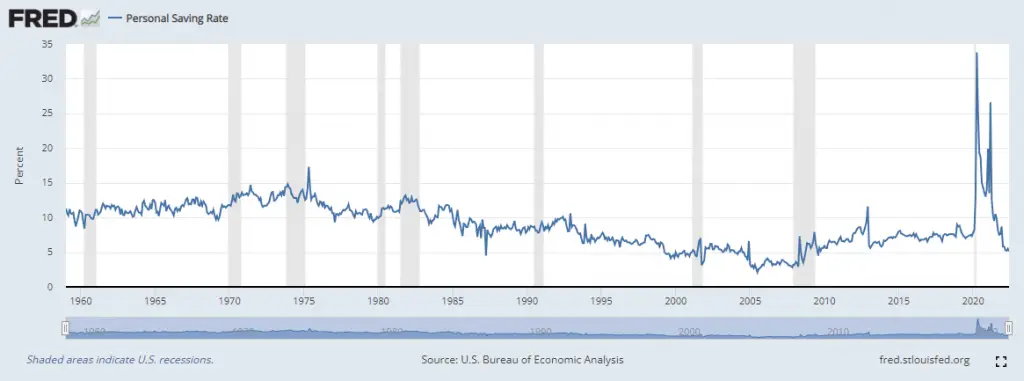

The “personal saving rate” is at 5% at the time of writing. This means that most people only save 5% of their income:

Looking at the chart above, we see that people used to save ten to fifteen percent of their income in the 60′ and 70′.

Somewhere in the 80′, people slacked on their savings, slowly decreasing to less than five percent.

In the pandemic, it shot up to 30% briefly but fell back to five percent in 2022 (which is the time I’m writing this article).

At no time have Americans (on average) saved 20% of their income over a significant length of time. This suggests that it’s hard, and takes a great deal of discipline.

We can therefore say this:

Saving 20% of your income is much better than most people. But more digging is needed before conclusions can be drawn.

View my calculation of the actual USD amount people on average save per month in this article.

Let’s move away from “most people”, and focus on YOU. We’ll now look at what factors we need to consider, and what outcomes you can expect from saving 20 percent of your income.

It largely depends on the following factors:

- Your financial goals

- Your family situation

- Your age

- Your current savings

- Your income

Let’s begin with goals and work through the list systematically:

How much to save depends on your financial goals:

I firmly believe in “beginning with the end in mind”. It only makes sense first to figure out where to go, before planning how to get there.

In doing this, we also have to consider another factor, mainly family situation.

Generally speaking, there are two different types of financial goals: Long-term and short-term.

By “long-term”, I mean retirement goals. What type of income do you want after retiring?

By “short term”, I mean saving for traveling, a new car, a downpayment on a new home, etc.

The most important goal when discussing the sufficient personal savings rate, is the long-term one. It’s what we’ll focus on in this article.

Ask yourself this: What income is sufficient for me after retirement?

To answer this in a meaningful way, think about these three things:

- Do I want a big house?

- Do I want a luxury car?

- Do I want to travel a lot, and generally do a bunch of “stuff”, or am I happy to stay at home and just relax?

Aiming for $100K a year is a good idea if you want a somewhat luxurious retirement. That’s based on an article I wrote about what making $100K per year is like, and what lifestyle it affords (for single people and families of four).

I think $40K per year is relatively comfortable for frugal people.

On average, here are the largest expenses retirees have:

| Item | Monthly Expense | Annual Expense |

|---|---|---|

| Housing (Mortgage, rent, property taxes, insurance, maintenance, etc.) | $1,456 | $17,472 |

| Transportation (Car payments, insurance, gas, bus tickets, taxi, etc.) | $624 | $7,492 |

| Healthcare (Health insurance, medical services, supplies, and drugs) | $569 | $6,833 |

| Food (Groceries, drinks and eating out) | $550 | $6,600 |

| Utilities (gas, electricity, water, phones, Internet, etc.) | $318 | $3,810 |

| SUM: | $3,517 | $42,207 |

The minor stuff is not that important, at least not for today’s purpose. Getting the big things right is what matters.

I’ll run an example throughout this article, and my financial goal for this example will be to have an annual income of $80K at the age of 65.

Suggested reading to further think about this:

- Can You Live On $4,000 Per Month? (Single and family of four)

- Living On $3,000 A Month – It’s Possible!

- Yes, You Can Live On $2,000 A Month! Here’s How & Where:

With that in mind, let’s move on.

How much to save depends on your age and current savings:

Generally speaking, the further away from retirement you are, the less you have to save.

That does NOT mean you should save less if you’re young, just that you don’t have to.

In the running example, I’ll be a 30-year-old guy planning to retire at 65. This gives me 35 years to save enough money to earn an annual income of $80K.

If you’re 40, you’ve got 25 years. If you’re 50, you’ve got 15 years, and so on.

By “the four percent rule“, I need to save up this much before retirement:

$80,000 / 0.04 = $2,000,000.

Simply divide your target annual income by 0.04. This will give you your target retirement savings.

Here’s a table showing how much you need to save for different annual incomes:

| Annual Income | Savings Required |

|---|---|

| $100,000 | $2,500,000 |

| $90,000 | $2,250,000 |

| $80,000 | $2,000,000 |

| $75,000 | $1,875,000 |

| $70,000 | $1,750,000 |

| $65,000 | $1,625,000 |

| $60,000 | $1,500,000 |

| $55,000 | $1,375,000 |

| $50,000 | $1,250,000 |

| $45,000 | $1,125,000 |

| $40,000 | $1,000,000 |

Keep in mind that this does NOT consider social security and such. Social security income would be added to the income generated from your savings.

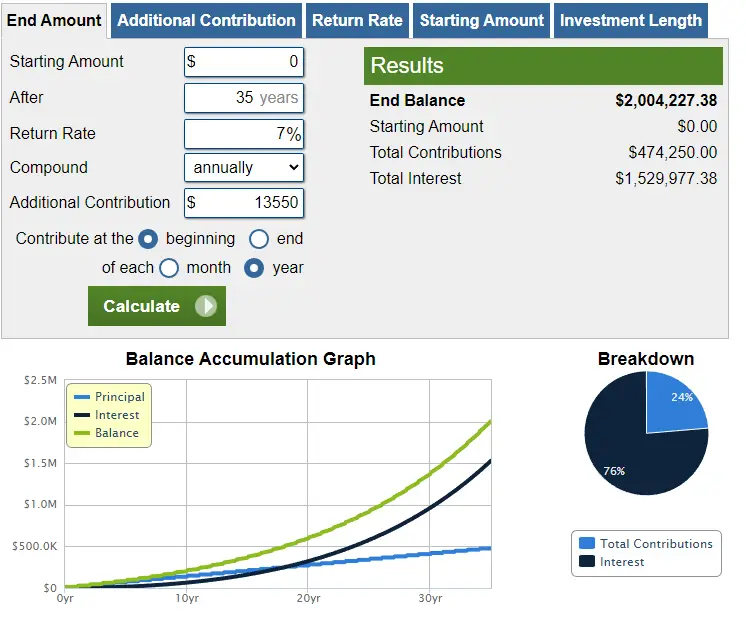

Let’s continue with my example. Remember, I want $80K/year and have 35 years to get there.

Based on the table above, I need to save up $2,000,000 minus my current savings in 35 years.

How much, then, do I need to save per year?

Well, when I say save, I actually mean invest. After all, saving money can’t make you rich, but investing can.

Assuming I have absolutely nothing saved up yet, an average return of 7% per year, and not thinking about 401K, tax, employer matching, and all that stuff, I need to save $13,550 every year:

You can use that calculator to play around with the “starting amount” if you have any funds saved for retirement already.

Keep tweaking the “additional contributions” until the “End Balance” reaches your goal.

To learn more about saving money, you can check out one of these articles:

After finding your target annual savings, you have what you need to figure out if saving 20% of your income is enough:

Finally, is twenty percent of your income enough?

With my goal of having $80K in annual income, I needed to save $2,000,000 in 35 years. According to the calculator, I need to contribute $13,550 yearly to my savings to reach that.

In that case, I need to earn $13,550 divided by 0.2 every year:

$13,550 / 0.2 = $67,750

In other words:

If I make $67,750 or more yearly, saving 20% of my income is enough to reach my financial goals.

Here is what you need to do:

Take your target annual savings (based on the calculator and your goals), and divide the number by 0.2. If the answer is higher than your annual income, saving twenty percent of your income is not enough.

Another way to do it is to multiply your annual income by 0.2. If the answer is lower than your target annual savings, 20% is not enough.

Here’s a table showing how much 20% of different annual incomes are, and what it will turn into over 35 years:

| Annual Income | 20% Of That | Invested Over 35 Years | Retirement Income |

|---|---|---|---|

| $100,000 | $20,000 | $2,958,000 | $118,000 |

| $90,000 | $18,000 | $2,662,000 | $106,000 |

| $80,000 | $16,000 | $2,366,000 | $94,500 |

| $75,000 | $15,000 | $2,218,000 | $88,700 |

| $70,000 | $14,000 | $2,070,000 | $82,800 |

| $65,000 | $13,000 | $1,922,000 | $76,800 |

| $60,000 | $12,000 | $1,775,000 | $71,000 |

| $55,000 | $11,000 | $1,627,000 | $65,000 |

| $50,000 | $10,000 | $1,479,000 | $59,000 |

| $45,000 | $9,000 | $1,331,000 | $53,250 |

| $40,000 | $8,000 | $1,183,000 | $47,300 |

You’ll probably not put all your savings into retirement savings, so the numbers above are kind of optimistic.

You’re more likely to put something like 10-15 percent of your income into long-term savings, and the rest into short-term savings.

For example, you might want to put some money away for a trip. Or maybe you’re trying to get a new car or pay down some debt.

Nevertheless, saving 20% of your income goes a long way, and in most cases, is enough.

Suggested reading: The 4 Steps To Save A Lot Of Money Fast

Conclusion: Yes, Saving 20% Of Your Income Is Enough

For most people, saving 20% of their income is enough. It’ll ensure you a comfortable retirement and you’ll have some money for short-term stuff like traveling and getting a new car.

To figure out if it’s enough for you, do this:

- Set your long-term financial goal. Specifically, what annual income would you like after retirement?

- Divide your target annual income by 0.04 to get the appropriate target retirement savings. This is based on a four percent safe withdrawals rate.

- Use this calculator to figure out how much you need to save yearly to reach your savings target by the age you want to retire.

- Divide the required annual savings by 0.2. If the answer is less than your income, saving 20% is enough. If the answer is higher than your income, saving 20% is not enough.

I hope you found this helpful. Good luck!

– Oskar