Inflation is making your money worth less, which is why you need more of it every year. But, is saving or investing the best way to deal with inflation? First, here the quick answer to “save vs invest during inflation”:

Historically speaking, a combination of saving and investing is best during high inflation. Invest for the potential upside and save to minimize the risk of the investing.

Now, let’s dig a little deeper. I find inflation interesting and think questions like this are important to answer. Writing this in July of 2022, the year-on-year inflation rate just hit 9.1%, making this question more relevant than (almost) ever! (source)

Suggested reading: Yes, Saving $1,500 A Month Is Good! (and how to do it)

Saving vs Investing Under Inflation: Risk vs Reward

We should first discuss the different risk/reward proposals of investing vs saving. Now, this is not only during inflation, but it’s especially prudent during times of high inflation, and losing money is even worse.

Typically, you’re told to invest if the timeframe is more than five years. This is because the stock market is likely to go up over a five-year period, even if it crashes at some point within those five years.

That means that even though the risk of a market crash is relatively high, the expected reward is even higher.

Whenever the expected reward outways the risk, and there are no better alternatives, the math says you should do it.

So, here’s the question:

Does the risk/reward of investing vs saving change during times of high inflation?

To answer this question, let’s look at historical data.

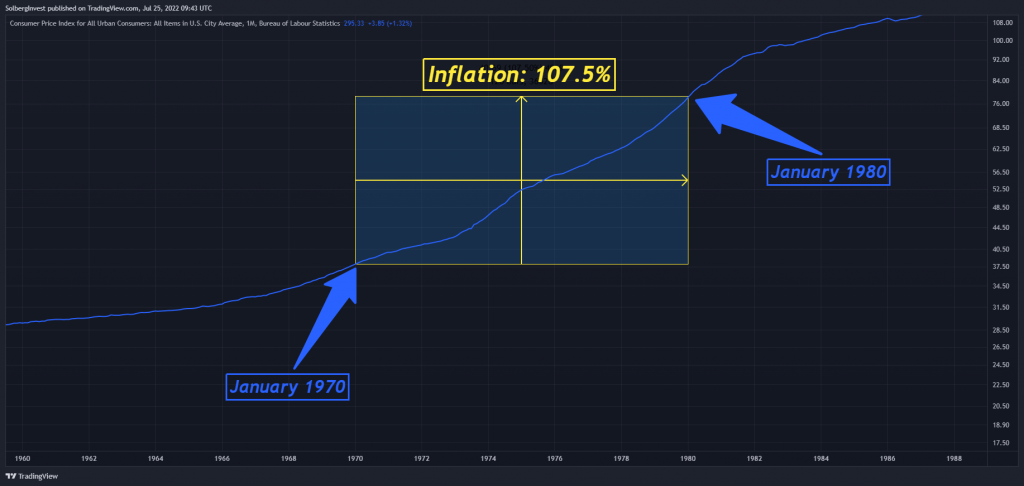

Specifically, let’s look at the inflation and The S&P 500 during 1970 – 1980.

Inflation during the 70s: 107.5%

The chart below shows the inflation during the 70s:

There are many ways to measure inflation, but for this article, we’ll use the “Consumer Price Index For All Urban Consumers (CPI-U)”, as it best fits most people. (source)

“How can inflation be 100%? Did money lose 100% of its value? Makes no sense bro…”

Inflation does not specifically mean “value of money”, but more accurately tells you the average price increase of “everything”.

Inflation of 100% means that “everything” has doubled in price. This is equivalent to saying that your money is worth half as much as it was before the inflation of 100%.

So basically, 100 USD earned in 1970 was equivalent to 200 USD in 1980.

We can now say this:

Saing money during the high inflation of the 70s would result in a 50% reduction in purchasing power. That’s the equivalent of having a return on investment of negative 50%.

Basically, savings had a return of negative 50%. To figure out whether it’s best to save or invest during inflation, let’s check out the S&P 500 and see if it did any better:

Investing During Inflation: 1970-1980

The chart below shows how the S&P 500 did from 1970-1980:

The S&P 500 only increased 15% over ten years. That’s not good at all. In fact, the inflation-adjusted returns make out to be (1.15 * 0.5) – 1 = -0.425. That’s right, you read that correct:

Investing during the high inflation of the 70s would result in an inflation-adjusted return, after holding the investment for ten years, of negative 42.5%.

A negative 42.5% return is better than a savings return of negative 50%. So, the “reward” of investing instead of saving was definitely higher during this particular inflationary period.

Now, just because the reward was higher, doesn’t mean it’s a closed case. We also have to look at the risk!

What if, for some reason, you needed to cash out your investments in 1974? Maybe there was a medical crisis, or you had to move because you lost your job.

If you had to cash out and sell your stocks in the S&P 500 in 1974, and keep them in a bank account until 1980, your return would be negative 35%. Inflation-adjusted that turns out to be -67.5%.

In other words:

Investing during the high inflation of the 70s, you took the risk of having a negative 67.5% inflation-adjusted return, which is much worse than saving.

Conclusion From Historical Example:

Looking at the historical example from 1970-1980, this is what we can conclude:

The rewards from investing during inflation are likely higher, given that the timeframe is long enough. However, the risk is much higher as well. Minimize the risk by investing only the money you know you’ll never have to cash out prematurely.

Saving vs Investing: Why Not Both?

Investing during inflation has the potential to reward you more than saving. But, as shown above, the risk is also higher.

Personally, I’m rather risk-willing. What I do during these inflationary times is this:

Save up a safety net of 6 months worth of expenses. After saving up six months of living expenses, I keep saving 8% of the value of my safety net every following year. This makes up for inflation and keeps my safety net safe.

Whatever money is left after saving I invest. Specifically, I invest in broad index funds, real estate, and cryptocurrency.

Well, I don’t “invest” in real estate, but I own an apartment on which I’m making monthly payments.

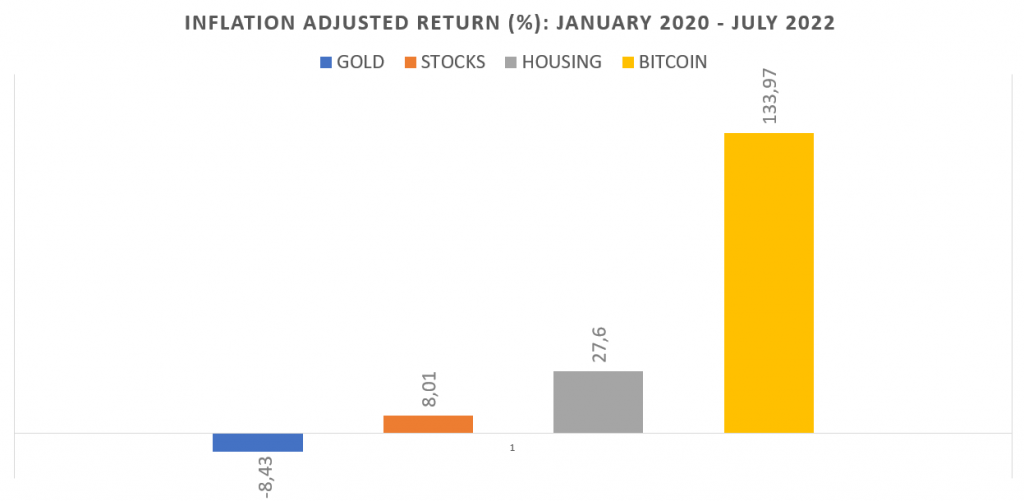

I see many people recommending Gold as a hedge against inflation, and I agree in principle. However, since the beginning of the current inflationary period, Gold has underperformed other major asset classes.

In my article about investing during inflation, I put together this absolute beauty of a chart (I love charts):

As you can see, Gold has underperformed, netting a negative return of 8.43 when adjusted for inflation.

Of course, the historical performance does not necessarily indicate future performance. For all we know, Gold might do better than all the asset classes in the next few years.

Still, the chart above shows the huge potential upside of investing during inflation. This is why I invest all my leftovers, after filling up my savings.

Conclusion: Combine them!

Investing during inflation has a higher expected reward than saving, given a timeframe longer than 3-5 years. However, the risk is also higher.

I’m not a financial advisor, and this is just my personal opinion, but this is what I think about the matter:

Both investing and saving during inflation are good. Save 6 months’ worth of expenses, add 8% to your saving every year to fight inflation, and invest the leftover money in index funds, real estate, and cryptocurrency.

Suggested reading: