Saving money is all about consistency. Sure, saving $10K for a couple of years is good, but the real magic happens when doing it for a couple of decades. In this article, I’ll do some good ol’ math and look into the question, “is saving $10,000 a year good?”:

Yes, saving $10K per year is good. It will make you a millionaire in 30 years and generate a passive income of $100K per year after 38 years (given a 7% annual return).

I’m assuming that you’re investing your savings into a passive index fund (or something roughly equating it) with an annual average return of 7%.

Investing makes the money work for you instead of letting it relax in a bank account. This is essential to understand: Interest compounded over several decades distinguishes the rich from the poor.

If you’re trying to figure out how much to save every year, read this article instead: How Much Should YOU Save Per Year?

If you prefer monthly saving targets, read one of these articles instead:

Let’s move on to the fun stuff:

Will Saving $10K Per Year Make You Rich?

To figure this out, we first need to agree on a definition of “rich” and figure out our timeframe.

Although I like to define rich as achieving a certain ratio between net worth and spending, let’s just call a person with $500,000 in net worth “rich”.

As for the time frame, I’ll put that to 40 years. You might think that’s insanely long, but with the graph I’ll make, you can see the path from year 1 to year 40, making it adjustable to your specific timeframe.

Once again, I assume you’re saving your money in a passive index fund. I assume index fund because it’s the best way to invest for “retail” investors like you and me. (source)

The red lines make it easier to see when you reach important milestones as for the size of your portfolio.

- Saving $10K a year for 22 years will make you rich, defined as having $500,000.

- Saving $10K a year for 30 years gives you a portfoilo of over $1,000,000.

- After 39 year of saving $10K per year, you’ll have over two million dollars.

The blue line shows the returns made each year. Basically, it’s the passive income your hard-working money is producing. The green lines show when your portfolio produces over $100K per year:

After 38 years of saving $10,000 per year, your portfolio will produce a passive income of $100,000 every single year.

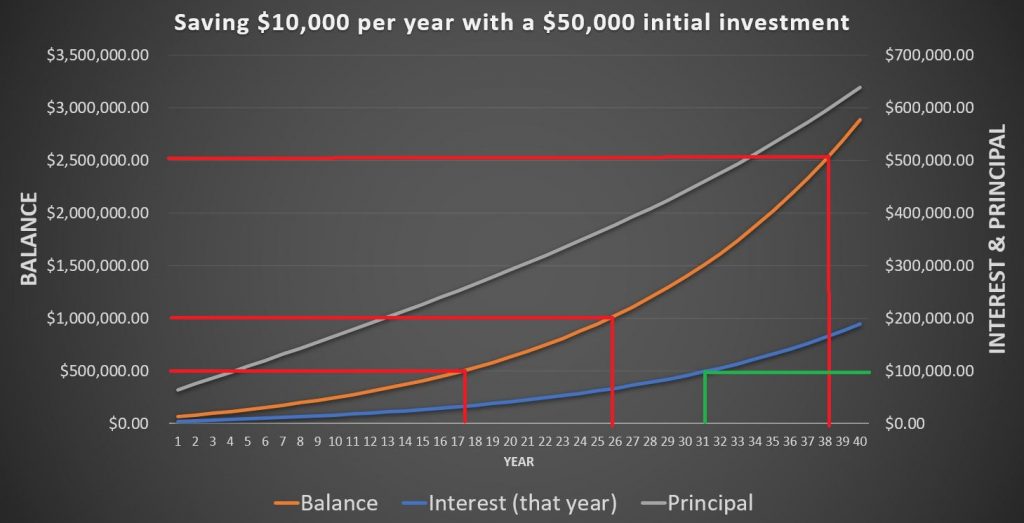

Saving $10K Per Year With a $50K Starting Point

Let’s say you already have some money saved up, like $50,000. How will that change your trajectory over the next 40 years?

Well, I’ve rerun the numbers. With the initial investment of $50K and saving $10K every single year, this is what would happen:

Results from saving $10,000 a year with a $50K starting point:

- You’ll have more than $500,000 after 18 year.

- After 26 years you’ll be a millionaire.

- Finally, after 38 years you will have $2.5 million in your portfolio.

- As for passive income, after 31 years your portfolio is generating $100,000 per year passivly.

Is It Possible To Save $10,000 Per Year?

Many people I talk to think saving $10,000 per year is unrealistic.

Please understand, that saving $10K per year doesn’t mean you have to put away exactly $10K once every year. You can save monthly, for a total of $10K per year. To figure out the best saving frequency, check out this article on how often you should save money.

Saving $10K is highly possible. It’s not that hard to achieve if you make the right moves.

What you need to do in order to make saving ten thousand dollars a month possible:

- Cut down your housing expenses. Housing is by far the biggest expense for most people. If you can cut down on this one, you’ll be able to save a lot more money. For example, if you spend $25,000 per year on housing, but you’re able to cut that down by 20%, you’ve got $5000 per year already – you’re halfway done!

- Cut down on commute-related expenses. This is often the next biggest expense people have. If you can cut this one down, you’re left with a big chunk of money to save every year. In The U.S, it’s normal to spend between $2,000 and $5,000 on commuting (source). If you’re able to cut this down by 33%, you’re saving an additional $660 – $1650

- Earn more money. The first steps you need to take are the two listed above – cut down on big-ticked spending. However, that’s not always enough. If you still can’t meet the $10K/year goal, you might need to increase your income. There are lots of ways to do this, but none are easy. I will not go into detail about it here, but a few examples would be: getting a second job, starting a blog (like this one), starting an e-commerce site, becoming a freelance writer on upwork or iwriter.

Pro tip: Move closer to work in a cheaper house/apartment. This cuts down on your housing expenses and makes getting to work cheaper and faster. It saves you both money and time, making it possible to save thousands of dollars annually!

Most people think it’s about cutting down on the “small stuff” like the Netflix subscription or the occasional Starbucks coffee. This couldn’t be further from the truth…

Small things have a small impact. Big things have a big impact!

Suggested reading: Is Saving $1000 Per Month Good

2 Ways To Invest $10,000 Per Year, Other Than Index Funds

Please understand this: If you’re not interested or passionate about finance, investing, or money, you should stick to index funds.

If you’re an average guy or gal, you should automate your saving/investing and never look back.

However, if you’re like me and find this stuff interesting, you might also want to dip your toes into other markets.

I’m a relatively young guy, so I might risk talking about stuff I’ve never had experience with. For example, I’m just now in the process of buying my first piece of real estate, but I’ve been reading books on it and talking with people for years. Please keep that in mind as I start discussing the three different markets down below:

Real Estate (The right way)

Investing in real estate is not a “new” thing. We’ve all heard that “real estate has created more millionaires than any other market.”, and that’s true.

There are two types of real estate investors: The professional and the amateur.

The professional buys as much real estate as possible with as high leverage (credit/loans) as possible. Basically, (s)he’s all in on this thing.

On the other hand, the amateur is only doing real estate on the side. It’s only part of a strategy to reach a broader financial goal or target. It’s more of a well-paying hobby than it is a job. (S)he wants to invest in one or two pieces of real estate, may do some repairs, and rent them out to generate a nice monthly income.

If you’re a professional, I can’t teach you anything. If you’re amongst the amateurs, there’s one thing I would like to pitch: House Hacking.

House Hacking means buying a piece of real estate where you can live while simultaneously renting out parts of it.

Done right, House Hacking can potentially eliminate your housing expenses, which is a huge deal when trying to save $10,000 per year.

Now that you’re House Hacking, eliminating your housing expenses, you can either choose to buy another piece to rent out or put the extra money into index funds.

After all, you’re already exposed to the real estate market through your House Hack, and diversification is recommended.

Crypto Currency Investing (Without the hype)

Personally, I’m deeply invested in the cryptocurrency market. In fact, this website started as a pure cryptocurrency blog. It has expanded into more general topics around saving money, early retirement, and other stuff I’m passionate about.

If you, like me, want to achieve higher returns than 7% per year, you can start to look into cryptocurrencies.

Know this:

If you’re able to put in the work and educate yourself about this incredible market, you can make mind-bending returns. The volatility and risk are much higher than traditional investments like passive index funds, but so are the potential returns.

For example, the cryptocurrency market surged in the first half of 2021. Many people, me included, made several-hundred-percent returns in a few months. Some investments even made several thousands of percent returns. After the surge, there was a 50% crash in two weeks, which was brutal…

Do you see how the crazy volatility offers unparalleled opportunity? Good luck finding another market where 250% gains in a few weeks are considered “pretty good” returns.

The right way to invest in cryptocurrencies for beginners is to DCA (dollar cost average) into the biggest coins like Bitcoin, Ethereum and Chainlink, and stay away from the hyped-up smaller coins.

For example, you could automate an investment plan to put $200 into Bitcoin and $75 in Ethereum every month. Do that for five years, and you might have gained a 10x, maybe even 20x on your money…

Keep in mind that the risk is high. Do not put all your money into crypto. Keep most of your money in safer stuff like real estate and index funds, and let crypto be the “spice” in your portfolio.

To learn more about crypto investing, you can read some of my articles on it. You can find a list of them here: cryptocurrency articles.

Conclusion: Yes, saving $10K per year is good

If you save $10K per year for 22 years, with a 7% return per year, you’ll have a portfolio of $500,000. After 30 years, you’ll be a millionaire. After 39 years, you’ll have two million dollars.

It’s far from impossible to save $10K per year. You need to cut down on significant expenses like housing and commuting to achieve it. Big things have big impacts, and small things have small impacts!