The Fat FIRE movement is for people wanting to retire early with an above-average lifestyle. If you’re considering joining it, you’re probably wondering what’s the best way to start and progress without default.

Here’s the short answer:

Fat FIRE is having 25 times or more of your expected annual retirement expenses to cover an upscale retirement lifestyle. To reach the Fat FIRE portfolio level, you’ll need to save 40 to 50% of your income and have 80 to 100% investments in stock.

Though the Fat FIRE bar is high, it is achievable with an above-average strategy. This article is a step-by-step guide to moving from zero to Fat FIRE.

Most people define FatFIRE as spending at least $100K a year in retirement without worry. I think it’s more subjective than that. I think the dollar amount isn’t that important, but the “without worry” part is what makes it FatFIRE.

For example, if you’re naturally frugal, you’ll feel “fat” on a $60K annual budget. If you’re more materialistic and want three expensive cars, a huge boat, and a vacation home in Spain, you’ll need to go much higher than $60K a year. My point is that FatFIRE is a subjective thing and that the numbers will vary from person to person.

This article will guide you to your definition of FatFIRE, no matter if that means spending $60K a year or $350K a year.

For a guide on LEAN Fire, check out this article instead: The Ultimate Guide To Achieve LEAN FIRE: (Step-by-Step)

Step 1: Fat FIRE Background Check

The high amount of savings required for Fat FIRE may make you feel jaded and as if your dream is unachievable. However, it begins with being authentic about your financial situation and planning tactfully to avoid pitfalls and challenges that might come along the way.

After completing this step you will have an overview of your finances. This is essential because without knowing where you are it’s impossible to decide where to go. Therefore, we will go through all the big financial positions you have, and end step 1 by calculating your net worth.

I will also give you some pointers at each stage to help you improve, but the focus should be to assess your current financial position.

Here is what you should consider:

Your Debt Level

It is normal to have some debt lurking around. However, too much debt can cripple your financial health because the payments cripple your ability to pursue other financial goals. Before joining the Fat FIRE movement, you should evaluate your debt-to-income ratio.

This ratio compares your monthly income to the amount you spend on debt.

You calculate your debt-to-income ratio by adding all your monthly debt expenses and dividing it by your gross monthly income before taxes. You then multiply by a hundred to express it as a percentage.

According to the Consumer Financial Protection Bureau, your debt-to-income ratio should be 36% or lower. A higher ratio is alarming and may hinder you from meeting Fat FIRE goals. You could take the following steps to lower your debt-to-income ratio:

- Pay off high-interest debt (above 7%) as soon as possible. This should be your number one financial priority.

- Reduce your credit card charges and postpone taking on more debt. Stop spending money you don’t have. If you can’t pay off your credit card monthly, you’re not ready to use a credit card.

- Refrain from making large purchases that could prompt you to use credit. If you really want a new TV or a new car, but you have to take on a bunch of debt, you should NOT do it. This is one of the best ways to fail to reach Fat FIRE.

Once you’ve lowered your debt-to-income level to a manageable level, you can direct your attention to Fat FIRE.

Fat FIRE seekers should aim to get their debt-to-income ratio below 15%. This will greatly better your monthly cashflow and allow you to save and invest much more than other people.

oh, and increasing your income will also better the ratio. If you’re unable to decrease your debt payments, you should therefore focus on making more money.

Your Savings

Check how much you have accumulated in your savings account. Your cash position should be enough to meet your short-term expenses and emergencies. The golden rule is to have three to six months of expenses saved in cash in case of an emergency.

Your monthly cashflow largely determines the amount that goes into your savings/investments. The easiest way to increase savings is therefore to increase cashflow.

To increase your cashflow, and consequently your savings, you either need to make more or spend less. The most effective and easiest way is to cut spending. You can either cut on fixed expenses or variable expenses.

Fixed expenses are the expenses that recur every month and whose costs are predictable and less prone to fluctuation. Variable costs, on the other hand, vary depending on your level of consumption of a good or service.

The hands-down best move you can make to increase cashflow and save a lot of money is to drastically cut down on the large fixed expenses. This takes sacrifice, but it is the best way to cut expenses.

This is my basic philosophy when it comes to personal finance: “Small things have a small impact. Big things have a big impact”.

By cutting down on large fixed expenses, you’re making a big impact on your finances, and the impact lasts because the cut expenses stay cut due to their fixed nature.

You can read more about how to save a lot of money in this article: The 4 Steps To Save A Lot Of Money Fast

Your Investments

Once you begin to Fat FIRE, a massive chunk of your paycheck will go to your savings and investments. Having a good investment portfolio is the key to reaching Fat FIRE. Reviewing your asset allocation will direct you on how much risk you bear and the potential returns you’ll reap.

In addition, it reveals to you the investments that are performing poorly so you can reallocate them into other assets performing well to boost your returns. Also, you get to know which investments have high administrative costs that reduce profit.

Fo the following the evaluate your investments:

- List all your investments by their position size (dollar value). Include all the stocks you own, all mutual funds or index funds, cryptocurrencies, etc. Include your home if you own it, but subtract the percent of it that the bank owns. For example, if you have paid down 30% of the house, only list 30 percent of its value.

- Add them all together to find the total value of your investments.

- Figure out the returns on all the different investments for the past 12 months.

- Figure out the average return on all your investments. To calculate the average returns, you need to divide the current total value of your investments by last year’s total value. Subtract 1 from that number and multiply by 100 to get it in percent.

You now know the total value of all your investments and the average return of your investment vehicles. This allows you to evaluate them according to their performance and rebalance according to your goals and risk tolerance.

Your Income

Your total income comprises the amount you earn from your wages, salary, investment distribution, dividends, and employee bonuses. It is the positive side of your cashflow, and one of the most important factors in the Fat FIRE equation.

Fat FIRE requires aggressive saving AND a relatively high income. You should save 50% or more of your annual income. This necessitates that your income is high enough to meet your monthly expenditures with only a fraction of it.

In most cases, only individuals with six-figure salaries, such as physicians, lawyers, and software engineers, commit to Fat FIRE, but if you’re erning less it is still possible. By living extremely frugal, saving up to 80% of your income, or starting a side hustle and increasing your income, you to can achieve Fat FIRE.

If you’re earning to little to Fat FIRE, consider these two moves:

1. Move to a cheaper apartment/house closer to work. This will drastically cut down on your housing expenses and your transportation expenses. On average, these two make up more than 50% of an American household’s monthly budget. By moving to a cheaper place closer to work, you can save much more money on a consistent basis.

2. Start a blog, like this one, about something you care about. It’s not hard, and only takes roughly 20 hours per week to get it to earn $1,000 a month in two years. Check out IncomeSchool’s youtube channel for getting started.

After completing both of the steps above, I managed to save 80% of my initial income (income before starting this blog).

Your Net Worth And Cashflow

Your net worth is a snapshot of all your assets minus liabilities (debts). A high net worth signifies financial health and goes a long way in reaching Fat FIRE.

You want to know your net worth because it tells you how well you’re doing financially, and how far away from Fat FIRE you currently are.

Your cashflow is a measurement of how much money you can allocate to investments and savings. It is crucial to have a strong positive cashflow to reach Fat FIRE.

Calculating Your Net Worth:

Evaluating your net worth helps you to determine where your money has been going and how you can redirect your spending to meet new goals. Traditionally, one includes basically everything in the calculation of one’s net worth. For example, if you’ve got a couple of golf clubs out back, you can technically count them as assets and add their worth to your net worth.

However, in this case, I think you should go by the definition of assets and liabilities in the book “Rich Dad Poor Dad“:

An asset is something that makes you money, by either generating an income or appreciating in value. For example, investments in an index fund are assets because the value appreciates over time. Another example is a rental property; it generates an income and appreciates in value over time.

A liability is something that is negatively affecting your finances over time. For example, your car is a liability because it cost more than it makes you.

With these definitions in mind, complete the following steps:

- Identify all your assets and assign a cash value to each. The cash value is the current expected value of your asset–not what you originally paid for it.

- Add the values to obtain your total assets. You may also choose to sort by liquidity of the assets, with cash being the most liquid and retirement funds being the least.

- Identify all your liabilities or debts, including their values. You can easily trace your debt amounts by checking your recent statements. Examples of liabilities include credit card balances, mortgages, and student loans.

- Add the values to obtain your total liabilities. You may choose to organize your debt by order of interest rates.

- Subtract the total liabilities from total assets to get your net worth. (Net worth = Total assets – Total liabilities).

You should do annual updates of your net worth. This is the easiest and most clear way to track how you’re doing financially.

Calculating Your Cashflow:

Calculating your cashflow is rather easy. Take your income and subtract your spending. Since you found your income in a previous section, you just need to calculate your current spending.

If you’re already budgeting, you already know your spending. If you’re not, follow these steps:

- Get a list of the last three months’ expenses. We want three months to get the average, as this is likely more accurate. Usually, this list can be found online at your bank. If you use a lot of cash, you can probably still find out how much cash you took out of your bank account in these documents.

Sort all the expenses into categories (categories are called “items” from here on). Examples of “items” are “Transportation”, “Housing” and “Personal insurance”. The expenses you can’t fit into any items, you put in the item called “miscellaneous”. - Sum up all the expenses in each item to find the total expenses for each item during the last three months. For example, if you had 25 different expenses of $10 each in the “Food” item, the total expenses for “Food” would be $250.

After finding the total expenses for each item, summarize all the items into a “Total expenses”. This should be how much money you’ve spent in the last three months. - Divide all the numbers from step 2 by three to get the monthly average. Since the numbers used are from three months and we’re looking for your monthly average, you need to divide them by three.

Now that you have estimated your average monthly spending, subtract it from your monthly income and you have your monthly cashflow. Alternatively, you can multiply your monthly expenses by twelve and subtract it from your annual income to get your annual cashflow.

Like your net worth, you should measure your cashflow annually.

Step 2: Setting Your Fat FIRE Goals

Setting clear, realistic, and measurable retirement goals should be the next thing you do after evaluating your financial situation.

When considering your retirement goals, you should consider the factors likely to influence your retirement spending. For example, if you have kids, your level of spending in retirement will be high compared to a person without a family or kids.

Also, your retirement lifestyle will significantly influence how much you need to save. If you want to change your house or place of residence, then your savings should be large enough to accommodate the costs. Likewise, your retirement target should be high if you want travel experiences and adventures.

As you’re looking to Fat FIRE, you probably want to have a rather luxurious life-style. This generally means double the median retieree expenses. In the next section, I’ll tell you how much that is, and later I’ll give you specific factors to consider to estimate it for your personal situation.

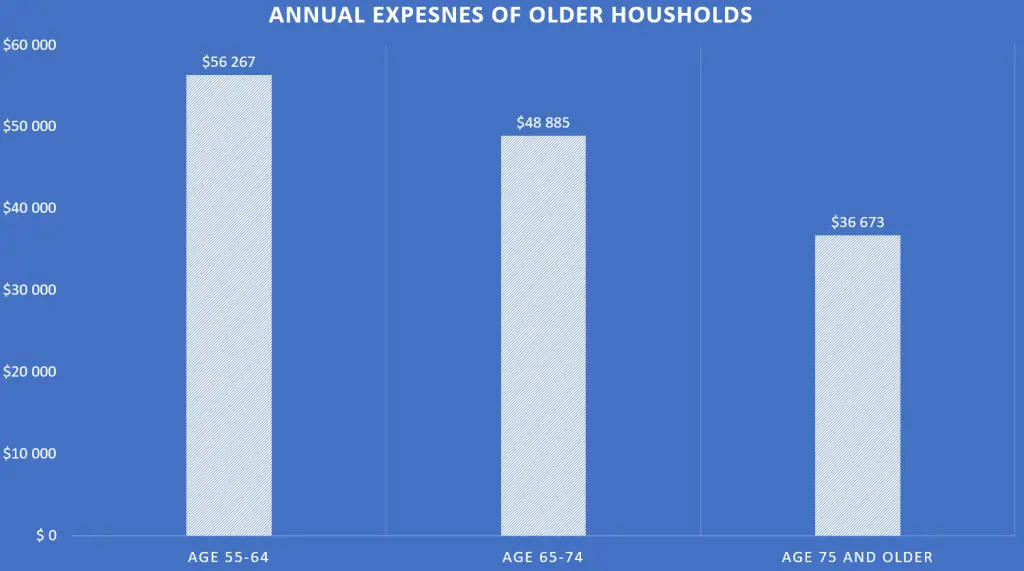

The Average Fat FIRE Retiree Expenses

Based on data gathered from U.S. BUREAU OF LABOR STATISTICS, I made a diagram showing how much older households spend:

A good estimate for your retirement expenses is double that of the ones above. This makes sure you’ve got plenty of cash to spend on luxuries like expensive travelling, cool cars, a big home and anything you might want (within reason, of course).

Another way id to look at the median household expenses in different cities. I made a table showing the median monthly expenses in 20 different cities in the U.S. for single people and families of four:

| Location | Median Expenses: (Single, Family) |

|---|---|

| New York, NY | $4,193, $7,934 |

| San Francisco, CA | $3,843, $7,471 |

| Oakland, CA | $3,403, $6,853 |

| Washington, DC | $3,113, $6,292 |

| Boston, MA | $3,268, $6,429 |

| Pittsburgh, PA | $2,178, $5,201 |

| Nashville, TN | $2,766, $5,740 |

| San Diego, CA | $3,118, $6,092 |

| Miami, FL | $3,086, $6,058 |

| Chicago, IL | $2,611, $5,506 |

| Philadephia, PA | $2,430, $5,307 |

| Los Angeles, CA | $3,044, $5,917 |

| Dallas, TX | $2,496, $5,286 |

| Atlanta, GA | $2,365, $5,117 |

| Las Vegas, NV | $2,130, $4,797 |

| Orlando, FL | $2,364, $4,979 |

| Austin, TX | $2,668, $5,264 |

| Huston, TX | $2,163, $4,762 |

| Tulsa, OK | $1,709, $4,115 |

| AVERAGE: | $2,834, $5,743 |

The key point is that the average of the median expenses for a single person is $2,834 and for a family of four it is $5,743.

If you double that, a single person looking to Fat FIRE will probably want to live on $5,668 per month, or $68,000 annually. Likewise, a family of four would need $11,486 a month, or $137,500 annually.

Now, if you’re able to pay off your mortgage and student loan debts before retiring, a huge part of the expenses counted in the medians above is cut. Therefore, a family of four could probably Fat FIRE on $100K a year, and a single person on $50,000, given that all significant debts are payed off.

Wether or not you should pay off your debt instead of investing more is a nuanced topic. To learn more about it read this article: FIRE Movement: Should You Pay Off the Mortgage or Invest?

With those estimates in mind, go over the following factors to get a better idea of your specific situation and goals:

Estimating Your Retirement Spending Needs

Even though the estimations in the previous sections are helpful, this is a step you cannot overlook when starting Fat FIRE. You need a rough idea of the amount that will comfortably support your livelihood. Without it, you can never figure out how much you need to save up before retiring, as the number depends entirely on your expected expenses.

To estimate your expenses, we’ll make a theoretical retirement budget. It’s not going to be a perfect prediction, but a reasonable estimate.

First, you’ll have to budget for your fixed expenses. Fixed expenses are the costs that recur every month and do not change with consumption. These are easy to predict because they do not fluctuate regularly. Examples of fixed costs include:

- Mortgage payments

- Rent

- Life and Health insurance premiums

- Childcare expenses

The second thing would be to determine your variable expenses. They are expenses that vary with your consumption. The costs increase when you use too much of a good or service. Unlike fixed costs, they are hard to predict because they keep fluctuating. Examples of variable expenses include:

- Travel

- Entertainment

- Clothing

- Food and dining out

The most realistic way to estimate your retirement expenses is to use your current costs as a benchmark. But because Fat FIRE supports a less frugal lifestyle, you should increase the costs accordingly.

The next thing would be aggregating the total fixed and variable costs. On top of that, you should add 30% to give an allowance for tax deductions on your retirement income and emergencies.

You might draw inspiration from the the median spending habits of U.S. households, as seen below:

| Item | Monthly Cost | Percentage of Budget |

|---|---|---|

| Housing (Rent/mortgage, utilities, etc.) | $1784 | 34.9% |

| Transportation (Car payments, gas, bus tickets, etc.) | $819 | 16% |

| Food (Groceries and restaurants) | $640 | 12.3% |

| Insurance & Pensions (Life insurance, pension savings etc.) | $604 | 11.8% |

| Healthcare | $431 | 8.4% |

| Entertainment (Subscriptions, speakers, new phone, etc.) | $243 | 4.7% |

| Savings | $190 | 3.7% |

| Apparel and Services | $120 | 2.3% |

| Education | $106 | 2.2% |

| Miscellaneous | $76 | 1.6% |

| Personal care | $54 | 1.2% |

| Other | $44 | 0.9% |

| TOTAL | $5,111 | 100% |

Tips To Help You When Estimating Your Retirement Expenditure

The following are some tips to better estimate your retirement expenses.

Plan Your Budget Based on Retirement Phases

Retirement has four phases with unique characteristics that may influence your spending. They include:

- Transition phase: This is the period you’ll be shifting from work to retirement. You might still have a part-time job or early retirement job. Though you’ll need retirement income, it might not be too high because you’ll have income from other sources.

- Early retirement: Leisure activities will increase in this phase because you’ll have more free time. It is the period where you’ll spend most of your retirement income.

- Late retirement: Your spending will likely decline in this stage as you start settling into retirement.

- End of life: Your spending is likely to spike in this period because of medical bills and long-term care.

Predict One Major Retirement Expense

Most retirement expenses may fall and rise evenly through the years. But you should anticipate at least one high cost, which can be:

- Purchase of a second home or a boat

- Education for your children

- Travel

Exhaust All Your Needs

Think through each category of your fixed and variable expenses to ensure you include every big and small cost you’re likely to incur. Use a spreadsheet to help you make a comprehensive list. This way, you’ll have all your needs covered in your savings.

Your Fat FIRE Number

Your Fat FIRE number is the amount of money/wealth you must accumulate to achieve financial independence. It’s a product of your anticipated expenses, which explains why we first predicted your retirement expenses.

There are two ways of calculating your Fat FIRE number (although they’re mathematically equivalent). Assuming a 4% withdrawal rate, which is the standard, the formulas are as follows:

1) Multiply your expected annual retirement expenses by 25.

2) Divide them by 0.04.

If you choose the safer option of a 3.5% withdrawal rate, you need to multiply by 28.5 or divide by 0.035.

If you’re really anxious about inflation, you might even drop your withdrawal rate to 2%. To calculate your FatFIRE number with a 2% withdrawal rate, multiply the expenses by 50 or divide by 0.02.

Let’s use an example to illustrate:

Assume that your expected annual retirement expenses are as follows:

- Fixed expenses $95,000

- Variable expenses $85,000

Let’s calculate your Fat FIRE number.

- Determine your total fixed and variable expenses.

Total fixed and variable expenses = Fixed expenses + Variable expenses ($95,000 +$85,000 = $180,000). - Add a 30% allowance for emergencies and tax deductions.

30% allowance = (0.3 x $180,000 = $54,000). - Calculate the total annual expenditure.

Total annual expenditure = ( $180,000 + $54,000 = $234,000) - Calculate your Fat FIRE number.

Fat FIRE number = Expected annual retirement expenditure / Safe Withdrawal Rate (4%).

Fat FIRE number = ($234,000 / 0.04 = $5,850,0000)

With your FatFIRE number calculated, let’s move to the final step of this guide.

Step 3: Create Your Financial Plan To Reach Fat FIRE

You know everything you need to know. All that’s left is to lay the plan. This step is by far the most exciting, as all the work from the past two steps starts to pay off and materialize.

We’re now ready to make an annual financial plan, and break it down into monthly targets.

Annual Plan to Reach FAT Fire:

Let’s break down your FAT Fire number into annual savings targets. I’ll lead with an example, and then give you the concrete steps to follow.

Example of creating an annual FAT Fire plan:

Going along with the previous example, my target for FAT Fire is $5,850,000 in savings and investments. As a 25-year-old guy, I want to retire in 25 years (within the age of 50).

So, I have 25 years to save almost six million bucks.

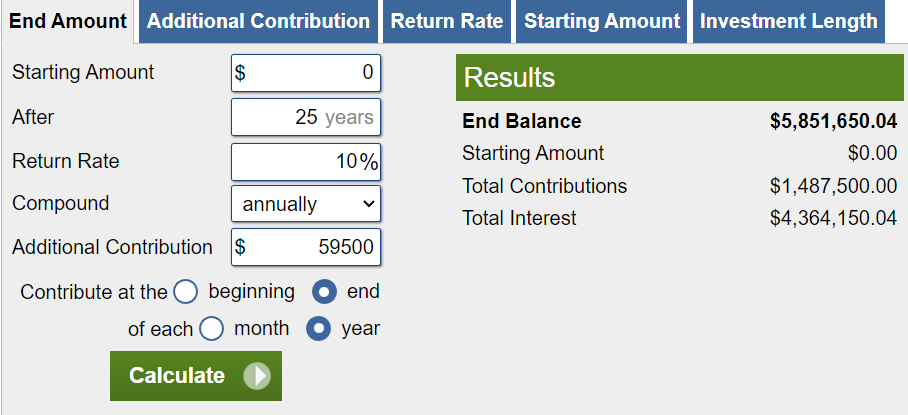

Now, I can’t just divide six million by 25, because that doesn’t take investment returns into account. What I need to do is to use a calculator and work backward.

Using this calculator, assuming a 10% annual return, I now know I need to save $59,500 annually:

To find your number, here’s what you need to do:

- Go to this website to find the calculator

- Adjust the input in “After” to the number of years you’re going to prepare for FAT Fire.

- Guestimate “Additional Contributions”, and make sure it’s put to “end” of each “year”.

- Press “Calculate” and check the “End Balance” in the top right corner. If the number is too low, increase the “Additional Contributions”. If it’s too high, decrease “Additional Contributions”.

Doing the four steps above, I figured out that I need to save $59,500 annually to reach my FAT Fire target. Do them, and find your specific number.

Breaking it down by month:

A monthly plan is often better than an annual one. The reason is that it’s easier to detect mistakes and calibrate accordingly.

To get your monthly savings target, just divide your annual target by 12. In my case, that’ll be $59,500 / 12 = $5,000 (actually $4,958, but I round up to $5,000).

Now I need to budget this as if it were a necessary expense, like rent or car payments. This way, I make sure that I’m able to reach my goal, and that I consistently save the required amount every month.

I’ll show you an example of a budget that is made for reaching FAT Fire. You should make something similar:

| Source (Income and Expenses) | Amount |

|---|---|

| Housing | $1,000 |

| Transportation | $400 |

| Food | $350 |

| Insurance | $200 |

| Clothes | $85 |

| Personal care | $100 |

| Subscriptions | $50 |

| Hobbies | $100 |

| Entertainment | $115 |

| Miscellaneous | $50 |

| FAT FIRE SAVINGS | $5,000 |

| Total Expenses | $7,450 |

| Monthly Salary | $6,500 |

| Side Hustle | $1,200 |

| Total Income | $7,700 |

| Income – Expenses (Monthly surplus/deficit) | $250 |

If you’re not making enough money to save at the rate required to reach FAT Fire, you either need to expand your timeframe or increase your income. Cutting costs is not the best move to reach FAT Fire. You should instead focus on making more money.

Consider switching careers, starting a side hustle, or joining a start-up. Look for opportunities where you can leverage your skills to a better degree than you are today. If you have no skills, consider spending some time and money on acquiring some. Just make sure the skills are valued by the marketplace!

By now you should have your goal written down, and your monthly budget leading to FAT Fire formulated. To finish off, let’s talk about where to place those savings to make them grow.

Best Ways of Investing for Fat FIRE

Since saving money can’t make you rich, you’ll never reach your FAT Fire number without it. I’ve written shortly about some of the best options below. Make sure to do thorough research before investing in anything, and do NOT think that the short paragraphs below are enough. They are mere introductions to the different investment vehicles.

Index Funds

Unlike mutual funds which are actively managed by a fund manager, index funds have passive management with the goal of matching the general performance of the market. This saves you from high operation fees and poor investment decisions made by managers trying to beat the market.

After investing, you pass other responsibilities to the manager, who looks to purchase and hold securities that correspond to the given index intending to match the index’s performance.

Index funds generally have the following benefits:

- High returns. It’s the nature of all stocks to fluctuate. However, index funds maintain a high average return of 7% – 10% depending on how far back you go to measure it.

- Diversification. You can own stock from various companies with a single purchase. For example, the Nasdaq fund exposes you to around 100 companies, and S&P 500 to about 500 companies.

- Low management cost. Because of passive management, the index fund expense ratio is low, which boosts your return.

Real Estate

For people with the right skills and mindset, real estate is a great long-term investment. If you’re handy, physical assets such as land, commercial, and residential properties can offer great returns and/or increased cashflow. Non-physical assets like Real Estate Investment Funds (REITs), and crowdfunding are other options for the investor with a more passive strategy.

The benefits you get from real estate investment include:

- Diversification. Real estate negatively correlates with other assets like stock, ensuring you’ll be able to withstand market fluctuations.

- Dual income. Your investment earns dividend income and returns on capital which helps supplement your income.

- High returns. The returns vary depending on the properties’ theme. However, the average return ranges between 5 to 12%.

The easiest way to invest in real estate is to pay off your mortgage. But that’s not always the best decision. To learn more about it, check out this article: FIRE Movement: Should You Pay Off the Mortgage or Invest?

Individual Stocks

Investing in individual stocks involves buying ownership of a company. If the company appreciates in value, so do your stocks. Many companies also pay some of their profits out to the shareholders. This is called “Dividend”. It’s a cash payment you receive just for holding the stock of the company. Dividend is a great way to increase cashflow or reinvest it in the company to increase your position further.

Although most people invest in mutual funds, individual stocks have a higher appreciation potential (and higher risk). In addition, individual stocks have the following benefits:

- No management fee. You incur zero management fee to own individual stocks, which means more returns.

- Control over your investments. Individual stocks give you control over which assets you want to invest in and where and when to invest.

- Tax advantage. You pay no tax on stock appreciation until you sell it.

Cryptocurrency

Crypto investing offers more risk, but higher potential returns than traditional investments like stocks and real estate. Bitcoin, for instance, has delivered an annualized return of 200% for the last ten years. It’s not likely to continue performing that well, but personally, I believe it has its place in the portfolio of risk-willing people.

For the tech-savvy, one can also look into cryptocurrencies other than Bitcoin, like Ethereum. Whatever you do, stick with the big ones like Bitcoin and Ethereum, at least until you’ve spent up to one hundred hours learning about crypto and finance. This market is brutal and shows no mercy for the ignorant.

If you’re interested in crypto, consider joining my free cryptocurrency newsletter:

I’ve got tons of articles about crypto on this website. In fact, initially, this website was built as a crypto blog. Check out the articles here.

The general benefits of cryptocurrencies are as follows:

- Potentially extremely high returns. Historically one can expect to make between 50 and 500 percent gains per year, depending on how deep into the crypto market you dive.

- Lots of innovative projects to learn about. The crypto market is full of innovative projects. For example, NFTs are cryptocurrencies. Other exciting sectors are DeFi and Metaverse.

- Can often be “staked” or blended out on dedicated platforms to generate a yield of 4% all the way up to 12% per year. This is kind of like dividends from stocks, but with higher payouts.

Final Thoughts

Achieving Fat FIRE is not for the faint-hearted. If you want financial freedom and to retire early, you must be ready to sacrifice your everyday luxuries for retirement. You’ll also need to be realistic about your finances, set achievable goals, and develop a sustainable strategy to meet those goals.

To reach FAT Fire requires that you make above-average money. You’re likely required to save multiple thousands of dollars every single month, which is impossible on a median salary. Consider switching careers, joining a startup, starting a side hustle, or learning some new, highly marketable skills.