Financial Independence, Retire Early (FIRE) is a movement that involves aggressive financial decisions. The movement aims to enable people to retire early so they can enjoy their lives without being limited by financial pressures. One of the initial decisions for FIRE enthusiasts considers is paying off their mortgages vs investing.

Here’s the short answer:

You should pay off your mortgage early if you are looking for long-term stability and your mortgage interest rate is above 4.5%. However, if your mortgage interest rate is less than 4.5%, and you’re not yet near retirement age, you should prioritize investing.

In this article, I’ll explore the pros and cons of paying off your mortgage or investing and help you decide which option you should focus on to meet your financial goals, so read on.

If you’re looking for a complete guide on achieving FIRE, check out one of these articles:

– The Ultimate Guide To Achieve LEAN FIRE: (Step-by-Step)

– The Ultimate Guide To Achieve FAT FIRE [2022]

Factors to Consider When Deciding Between Mortage or Investments

FIRE is a mindset that you can have financial freedom at any age, regardless of how much you make or how much debt you have. The goal is to be able to live off of the interest of your investments and not have to worry about working a job to make ends meet.

There are multiple ways to achieve financial independence, and people may choose which suits their situation best. One of these ways is paying off your mortgage or avoiding any other debt.

Deciding whether to pay down the mortgage or invest can be difficult for many people because it requires both financial knowledge and, most importantly, emotional intelligence. Being able to determine which option is best, right now in your life, can be challenging.

To decide between paying off your mortgage and investing, you should take into account the following six factors:

- The interest rate on your mortgage

- The appreciation of homes in the area where you live

- Taking into account your income tax rate

- The current market value of your home

- Taking into account your income tax rate

- A projection of inflation

- Estimated return on investment

Ultimately, the best option is the one that makes the most financial sense for your individual situation. Consider the interest rate of your mortgage and financial goals carefully to decide if paying off your mortgage will make more sense than starting your investments.

Reasons in Support of Early Payment of Mortgage

From a financial perspective, investing money rather than paying off a mortgage is usually better. Some people may choose to pay off their mortgage earlier because they feel it is important to be debt-free. Others may have different reasons for choosing to invest more.

While it is ultimately up to every individual to decide what suits their need, let’s look at the reasons and benefits of paying your mortgage earlier:

Better Monthly Cashflow

Paying your mortgage early can free up a lot of money each month, thereby reducing your monthly expenses. According to The Federal Reserve Bank of New York, by September 2021, Americans held $10.67 trillion in mortgage debt.

By paying off your mortgage early, your expected retirement expenses will decrease, making your FRIE number lower. In addition, you will have more funds you can invest on a monthly basis. Getting your FIRE number as low as possible is the fastest way to achieve FIRE. If you’re willing to live frugally, you can reach your FIRE number faster than you might think.

Savings on Interest

As you pay off your mortgage, the amount of interest you pay also reduces. This reduction in interest payments is because the total amount that you have to pay interest on is smaller, saving you a lot of money in interest payments.

This strategy makes economic sense if your mortgage interest is high, maybe above 4.5%. You can use the savings in interest to pay down other high-interest debt or even to save for retirement.

Think of it like this: If you’re paying off debt with a 4.5% interest rate, it’s like investing money with a guaranteed return of 4.5%. The stock market on average gives you 7% per year, but the return is far from guaranteed. So, you have to choose between a larger, but risky, return from investing or a guaranteed return from paying off debt.

A Sense of Emotional Peace

Being in debt is a source of stress for many, and your emotional state affects your financial decisions. Paying off your mortgage can offer a great deal of relief, especially when times are tough. You won’t be forced to choose between meeting your basic needs and making mortgage payments simultaneously.

Creating Equity

Home equity refers to the market value of your home after removing the value of any debts on your home, like the mortgage. A great way to increase home equity is to pay off your mortgage.

Home equity is important because it can give you a cash cushion for major purchases, debt consolidation, or home improvements. For many people, their home equity makes up a large portion of their net worth.

Basically, the principle portion of your mortgage payments is an investment in real estate. Combine this with the “saving on interest” section, and you’ll see how paying off your mortgage is a great investment – high potential returns on the principle (from appreciation on the property) and a guaranteed return on the interest payment (equal to the interest rate).

Disadvantages of Early Mortgage Payments

- Your wealth is locked up. While you can sell your home if needed, it’s not as easy as cashing in a stock or bond. Closing a sale can take months or even years. Real estate is a long-term investment.

- Paying off at the expense of other opportunities. The money you use towards paying your mortgage is money you’re taking away from other financial goals. Basically, the opportunity cost me be too high to justify.

- Missed tax benefits. There are tax benefits of having a mortgage. For example, all interest payments can be deducted from your taxes in most places.

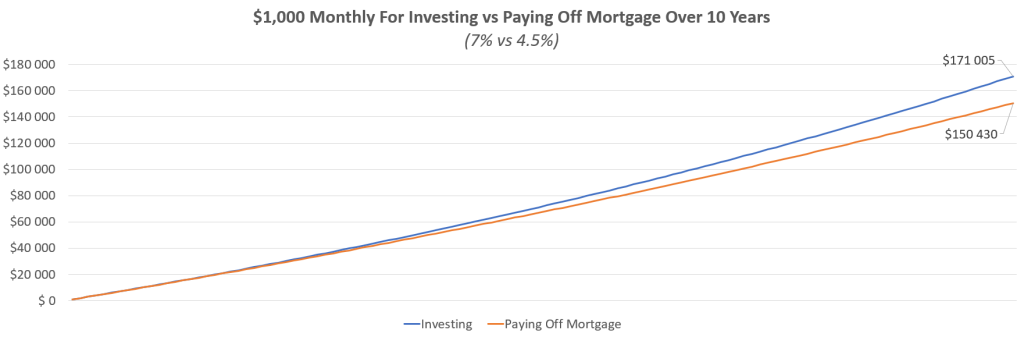

To visually show you how much more money you can make from investing at a 7% vs 4.5% annual return, I made a chart showing how investing $1,000 a month vs paying off $1,000 a month at 4.5% might turn out over ten years:

The difference comes out to $20,575 in this specific example. More generally, investing is likely to be 13.7% better than paying off your mortgage during a ten-year period.

That’s a lot. The additional $20,575 will continue to grow due to compounded interest. In the stock market, you can expect to double your money every seven years. That means the $20,575 you earned by investing rather than paying off the mortgage will turn into $41,150 seven years later, or $82,300 14 years later. Never underestimate the powers of compound interest.

Reasons in Support of Investing

Now that we’ve explored the pros and cons of paying off your mortgage, let’s look at the benefits of investing.

A Practical Method To Optimize Returns

Paying off your mortgage early could be influenced by emotions, but investing is considered the logical way to maximize returns. If you have a mortgage rate of under 4.5%, you’ll probably make more money investing instead of paying down your mortgage.

Historically speaking, investing in index funds offer 7% returns per year. This is likely much higher than your current interest rate. Therefore, it’s mathematically and financially better to invest rather than pay off (low-interest) debts.

Liquidity of Your Investment

It’s important to consider your investment’s liquidity when deciding where to put your money. Liquidity refers to the ease with which you can access your money. Investments are a great way to keep your funds liquid for emergencies or other financial opportunities.

Investments in stocks, index funds or bonds are much more liquid than your home. This is an advantage as you might need to sell quickly in case of an emergency or an unexpected move in the market.

Higher Return on Your Investment

Suppose you’re trying to decide whether to invest your money or use it to pay down your mortgage faster. Investments offer a better return on investment (ROI) than mortgages do, which is why most people starting FIRE are encouraged to invest as soon as possible.

The money you earn through investing can later be used to pay off your mortgage. This is the preferred strategy by lots of FIRE participants.

Disadvantages of Investing

While there are many reasons to invest over paying off your mortgage, it is important to be cognizant of the disadvantages of choosing to invest.

- A greater level of risk. When it comes to investing, there are different levels of risk. While the stock market may offer better returns, it does tend to have more volatile ups and downs than the housing market. This means there is a higher chance of losing money if you invest in stocks.

- You’re in debt for longer. There are several risks associated with mortgages, among which is the danger of foreclosure if you cannot make your payments. Taking out a mortgage means you don’t own your home until you’ve paid it off. Paying it off reduces the risk of losing your home in the event of a financial or personal emergency.

- No guaranteed return. There are no guaranteed returns when investing. Paying off your mortgage offers a guaranteed return equal to the interest rate on the loan. Although this likely is lower than the returns you’ll make on average by investing, it’s a factor to consider. Especially if you’re close to retirement age.

Conclusion: It Depends On Your Risk Tolerance And Age

There are advantages and disadvantages to clearing off your mortgage early and then investing. As an investor, you know that paying off your mortgage is regarded as a guaranteed return on your investment while investing always involves some element of risk.

However, investing can earn you much higher returns than paying off your mortgage, making it the better option for some people. The bottom line is that it depends on what is most important to you, and your personal risk tolerance and age:

Generally speaking, if you’re less than ten years away from retirement, I’d say paying off the mortgage is the best option. Investing is the better option if you’re more than ten years from retirement.

Independent of age, if you can’t stand risk and want to take the “safe” route to FIRE, paying off all kinds of debt is the first thing you should do.

If you’re a risk-taker, invest everything you can and pay as little on the mortgage as possible. You might even talk to your bank about only paying the interest and not any principal. This way, you can invest even more.