Blockchain is what we can call a “fundamental technology”. In isolation, it’s not all that exciting, but amazing stuff can be built on top of it.

Essentially, a blockchain consists of digital blocks of information about transactions, stored on a decentralized, public database (Ledger). This database, and the information it stores, is available to everyone with an internet connection.

That’s a mouthful…

I will break it down into digestible pieces, and stay away from fancy words only tech geeks know. I’ll do my best to keep your brain un-pretzeled.

Let’s go!

Blockchain Basics

The blockchain is essentially just a chain of blocks. The blocks are digital information like transaction details, and the chain is a public database. This chain of blocks is accessible to everyone with a computer and internet connection.

In other words, the blockchain simply is a chain of chunked-up information about transactions.

That’s it. Now you know what a blockchain is. A bunch of aggregated or compiled information stored in digital blocks, organized in a public database accessible to everyone.

Well, it’s more complicated than that of course, but it paints the picture. There are still a few details we need to go through, like exactly what the blocks contain, and how this “public database” works. Let’s start with the blocks.

The Blocks on the Blockchain

The blocks in the blockchain contain three parts:

1) The blocks store information about the date, time and the amount that was transacted. For example: Date:06.24.2019. Time: 13:43. Amount: 10.75USD

2) The second piece of information the block stores, is about the parties involved in the transaction.

Let’s say you send Bob 50 bucks. The block would then store the information about you as the sender, and Bob as the receiver.

The block wouldn’t store your real names,

but instead a string of characters, a “digital signature”, not unlike a username. This signature is called your “address”, and is different for everybody. It’s like a fingerprint, no one has the same.

3) The third piece of information stored in a block, is a unique “name” for itself, called a “hash”.

This name is a string of characters, unlike any other previously existing block. This unique string of characters is called a “hash” and it makes it possible to distinguish between different blocks on the chain.

To summarize, a block contains info about who was involved in the transaction, when the transaction took place, and how much was transacted. All of this info is stored in a block with a unique “hash”, which distinguishes it from other blocks in the chain.

It’s also important to know that one single block can store a few thousand of these transactions, to a total of around 1MB of data.

What needs to happen after the block has been filled up with transactions, is to add it to the chain:

Adding a New Block to the Chain

For a block to be added to the chain, there are a few criteria that need to be met:

1) There must be a transaction. Someone has to buy/send/receive something.

2) The transaction must be “verified” by a network of computers, called “miners”. The moment someone starts a transaction, the computers will check if the transaction is true – if it registered the way it actually happened.

In other words, they check if the details like the time and date of the transaction, as well as the amount, is correct.

The verification of transactions is an essential part of the blockchain.

We’ll get back to why this is the case later when we go over the security of blockchain technology.

3) Once all the transactions in the block have been verified, the block needs a hash, the unique string of characters.

An algorithm decides the hash of a specific block. The hash is not public data, so no one knows what numbers and characters the hash consists of.

The moment the block has gotten its hash, the network of computers will start guessing random numbers/characters until they guess the hash that the block got from the algorithm.

Once the network guesses all the characters in the hash correctly, the block becomes part of the chain. We call this process “hashing of bocks”.

When we add a block to the chain, it becomes available for everyone who wants to see it.

It’s transparent and free for anyone who would like to check it out.

Now that you know the basics of how the blockchain works, we can begin to explore its benefits:

Benefits of Blockchain #1

Security

Although blockchain data is available to everyone, some people choose to connect their computers to the network and help in validating transactions and hashing blocks.

Validating transactions and hashing blocks is the activity referred to as “mining”. When a miner guesses the correct hash of a block, they get a reward. Bitcoin miners receive rewards in BTC. Ethereum miners receive ETH.

The rewards act as an incentive for miners to secure the network by validating transactions and hashing blocks.

The more computers that work on validating and hashing, the more secure the network becomes.

Every computer that connects to the network (all miners) will receive live updates of the blockchain, kind of like a Facebook feed. When we add a block to the chain, every computer in the world connected to it will know.

All the computers also have a copy of every single block added in the past.

In other words:

All the computers have a copy of the blockchain, and they all receive live updates of it.

This is important:

No single one of these computers has “the right” copy of the blockchain. They are all equivalent, almost in a democratic sense.

If the network disagrees on the legitimacy of a transaction, the majority decides.

In other words:

For a transaction to be verified, over 50% of the network has to agree on its legitimacy.

This makes it extremely hard to manipulate the blockchain. If you want to fake a transaction, you’ll have to convince over half the network that it happened, which is hard.

The only way to do this is to dedicate more computing power to validating the fake transaction, than the legit computing power that knows it’s fake.

This means that if anyone wants to fake transactions, they need more computing power than all other miners on the network combined.

To execute a “51% attack”, as it’s called, on the Bitcoin network, one would have to buy enough miners (dedicated computers) to match the current “hash rate”. Let’s run the numbers.

How much does it cost to “hack” the Bitcoin blockchain?

To execute a 51% attack, you have to buy tons of Bitcoin miners to match the computing power of the current network of miners.

The most cost-effective way to do this is to buy “ASIC Miners”.

ASIC miners are “application-specific integrated circuit” machines, which means that the computer is dedicated to one this, and one thing only – mining Bitcoin.

You need to match the current “hash rate”, which is the measurement of the total computing power of miners securing the Bitcoin network.

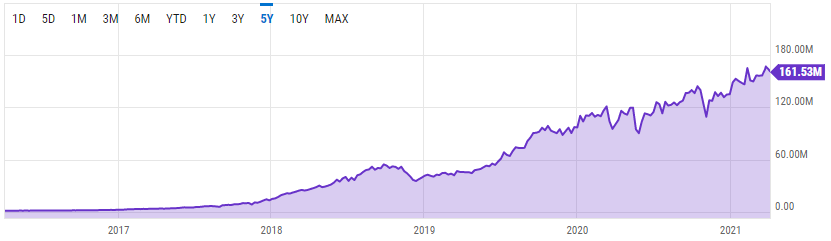

Below you see the current hash rate of the Bitcoin network:

Currently, the hash rate is at 161 million Terra hash per second. Let me write that number out, so you get an idea of how insanely large that is:

161 000 000 000 000 000 000 Hash/sec

Now, if you were to buy enough ASIC miners to match this number, you want to buy Antminer S19 Pro, as this miner gives you lots of power relative to the electricity it uses.

Each S19 gives you 110 TH/s. To reach 161 million TH/s you need to buy close to 1.5 million of these miners.

The cost of one single S19 pro is $8000.

1.5 million S19 pros would cost $12 000 000 000 – twelve Billion USD.

You would also need to buy containers, or warehouses to store these miners. You would also need to hire tons of electricians to set up the power supply.

For those reasons, we round it up to 15 Billion in hardware and set-up costs.

Let’s look at the electricity costs of keeping up the 51% attack:

One S19 pro uses 3250 watts, which costs approximately seven bucks per day, given that you get an institutional rate on the electricity.

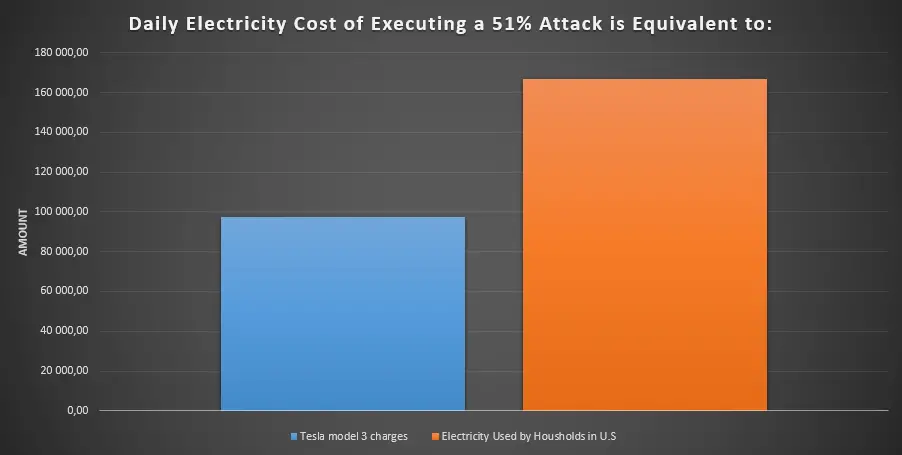

If you have 1.5 million of them, the power consumption would be 4875 MW (mega/million watts) and you would have to pay $10 500 000 per day.

To put that in perspective, I’ve calculated the number of U.S. households you could power, and the amount of Tesla Model 3’s you could charge with the same amount of energy:

Does 51% attacks on the Bitcoin blockchain pose a risk?

No, because executing a 51% attack isn’t worth it. The price tag of a 51% attack is not the only reason it’s highly unlikely to happen:

If someone successfully executed a 51% attack, the Bitcoin price would crash, leaving the attacker empty-handed. As soon as Bitcoin is hacked, it’s worthless, so why the heck would anyone invest 20 billion dollars to do it?

It’s not only faking new transactions that’s hard. Tweaking old ones is no easy task either.

If you want to manipulate a blockchain, you would have to manipulate every single copy of it in the network.

In Bitcoin’s case, this means that an attack would need to hack millions of computers to succeed, which is no easy task.

This is why we call the blockchain a “distributed ledger”. This is also why we call Bitcoin “decentralized”. Decentralized, meaning that there is no single database that keeps the “right” ledger, it’s spread out to millions of computers, all equally “right”.

Decentralization makes the ledger extremely hard to manipulate, and therefore extremely safe.

Benefit of Blockchain #2

Direct & fast

When you send money through a bank, you need to trust the bank not to lack security, not to make mistakes and you have to pay fees.

When you send money through Bitcoins distributed ledger, you do not need to trust anyone. The transaction goes directly from you to the receiver, without any intermediaries. This makes it fast, cheap and trustless.

This can obviously revolutionize the way we transact money, but in a broader sense, it could also revolutionize the way we transact information.

Transacting information simply means sending information from one place/person/institution to another.

When you send someone a snap, a mail, or a WhatsApp message, you send him or her information. When you set up a user on eBay or Amazon, you transact your information.

Now, let’s say WhatsApp gets hacked. The hacker would then be able to change the messages in the database.

The hacker could change the time and date, the senders and receiver, and what the messages contained. This is because the “ledger”, in this case, is centralized. If you change that one, you change it for everybody.

As you already know, if it had been decentralized, the attacker would have had to change all of the devices for the attack to be successful.

Another point to make here is that when you send a message to a friend on WhatsApp, or any other messaging platform, you’re not sending it to your friend:

You’re sending it to WhatsApp. After they have received the message, they send a message to your friend. Had it run on blockchain; the message would go directly to your friend, without WhatsApp as an intermediary.

This makes it so that you can transact information with anyone you want, without anybody else eavesdropping on your conversation.

This is highly relevant in these times, with Facebook and other giants eavesdropping more than most people find appropriate.

Look, I’m not a drug dealer, inside trader, terrorist, or anything of that sort. I’m not spilling confidential information, planning a bank robbery, or conspiring against Trump, but:

When I chat with my friends, I don’t like Facebook awkwardly standing in the corner of the room pretending he’s not there.

I find it worrying that Facebook and Google supposedly know me better than my best friends. I find it worrying that they make a profit by selling information about my digital behavior.

This is a deep problem that only seems to get worse over time. We need blockchain to solve this.

Did you know that there are different ways of “mining” called “consensus protocols”? Bitcoin uses Proof of Work, but is being threatened by other protocols like Proof of Stake. To learn more about this, check out this article:

Will Proof of Stake Kill Mining?

Educate Yourself

That’s only a few of the many things that make the future of blockchain technology so incredibly thrilling.

It truly has the potential to change the world as we know it.

Now that you know the basics of the technology, I urge you to keep reading about Bitcoin, and how it works. Given the facts that you’ve read this far, I know that you’d love this other article below.

It’s about how Bitcoin, using blockchain technology, might just overthrow the United States Dollar.

Check it out: