Central banks all over the world are printing money like drunken sailors, desperately trying to keep the economy floating. Make no mistake – this will affect your life, in more ways than you might think. It’s time to talk about inflation, and all the other consequences that follow.

In this article we will deep-dive into several topics, including:

1) How the economy works

2) What triggers a financial crisis and how we deal with them

3) Inflation, how new money is created, the consequences of money printing and inflation

4) How Bitcoin might be the solution to our problems.

We will go through all of this without using the “finance-words” you’ll get stuck on when trying to “google it”.

Actually, inflation is not that complicated, but it’s often misunderstood. Make sure to read through the whole article to get the full explanation, and deep understanding, of what inflation actually is.

These days, governments are handing out stimulus checks and emergency money to businesses like never before.

However, there’s no such thing as a free lunch…

How the Economy Works

Our economic system is built on people “spending” money. In fact, if people stop spending, the economy crashes.

For this reason, the economy is reliant on people earning money as well. After all, you need to earn money to spend money.

Later, we’ll go through what happens when a large number of people lose their jobs. We will conduct a thought experiment, and lead out the consequences that follow:

Spoiler alert; it’s going to be bad…

But first of all, let’s go through why spending is so important:

Your Spend = My Earning

When people stop getting their paychecks, they spend less money. When people spend less money, someone else earns less money.

This is important; your spending, is someone else’s earning.

When you buy groceries, or pay your rent. The money you spend is the money the store, or your landlord earns.

If you stop spending that money, they stop earning it. This is why it’s bad for the economy that people lose their jobs; they spend less.

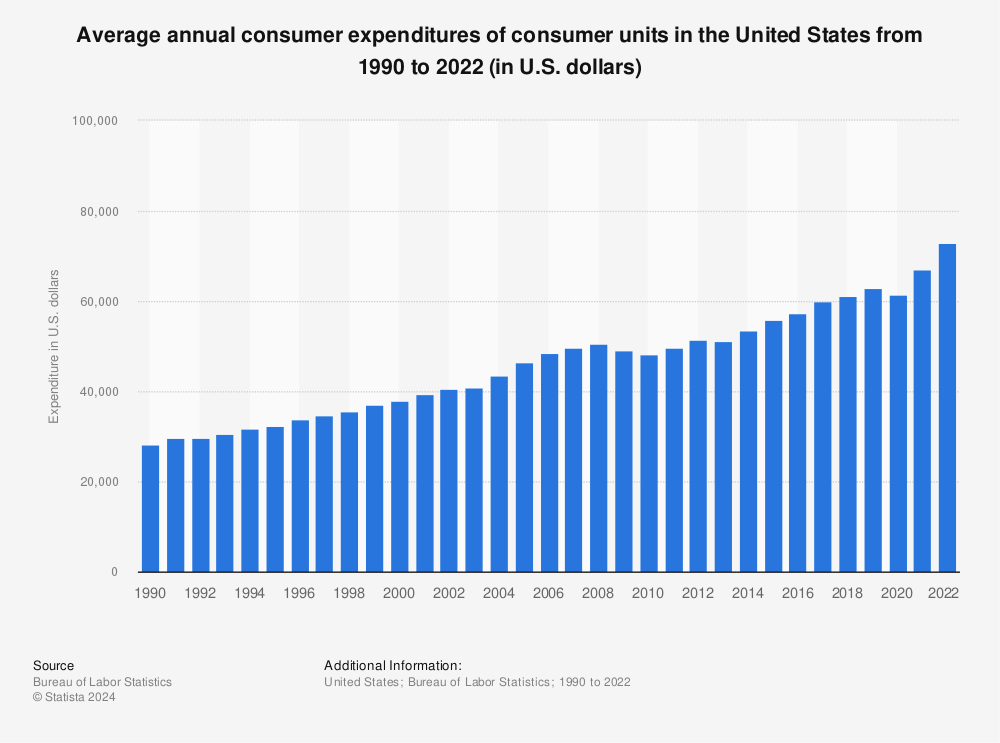

The total spending by the average person in United States of America has doubled from 1990-2019 :

Find more statistics at Statista

Credit – Spending on Steroids

If we add credit on top of this equation, things start to go crazy:

Let’s say you qualify for a loan of 1 million dollars, and you take it. You now have more money to spend then you had before.

The reader of this article might not spend this money on consumer goods right away, but the average person would probably manage to make a solid dent in the 1 million within a month.

We all know these people. As soon as they get their hands on some money, they spend it.

A fancy dinner, new tools, new clothss, a new car or even a new house.

Now, all this extra spending makes other people earn more. Remember, your spending is someone else’s earning.

When you spend one million dollars more than you actually have, this money (credit, to be precise) increases someone else’s earnings even more than your regular spending would.

When these people earn more, they’re not only able to spend more, but also to loan more.

They then get a bigger loan from the bank than they would have if you didn’t get the one-million-dollar loan.

In other words, the fact that you got a loan of one million bucks, makes other people able get higher loans.

This increases their spending as well, which increases someone else’s earnings, which increases their ability to loan and spend more as well.

Credit is like steroids to the economy.

It’s money that doesn’t exist, but increases your spending-power, and therefore what others earn, which leads to them acquiring even more credit.

This cycle then continues for a few years. The credit grows exponentially.

However, their actual productivity isn’t much higher than it was before the steroid injection.

The productivity is what should dictate your spending power/earnings, in a functioning economy.

We should, ideally, have resources/spending power in proportion to the product/services we produce.

Below you see the total debt of U.S citizens since 1990:

In the same time that the median income, as well as median spending, of Americans has (roughly) doubled, the total debt has increased with a factor of 5.24.

In other words, since 1990, debt has increased 2.62 times as fast as the income.

However, the population has increased with 32% as well, which only affect the debt (more people = more debt), but not the median income (more people does not equal a higher median income).

To make the right calculations, we have to adjust for the population growth:

The rate at which the debt has outgrown the median income is 1.98 times as fast, basically twice as fast, when adjusted for population growth.

All of this debt has increased the spending power of Americans drastically over the years, but the party has to end as some point…

The Triggers of an Economic Crisis and Causes of Inflation

Now that you understand that your spending is someone else’s earning, and that the cycle is juiced up on steroids because of credit, let’s look at what happens when we lose our jobs, or people just decide spend less.

Let’s lead out the consequences, and take it step-by-step on our road to financial doom and inflation:

Step #1 to a financial crisis and inflation

When people start cutting back on their spending, the first ones to feel the impact are businesses. They immediately start earning less. Their sales are declining, and they aren’t making as much as they used to.

This forces them to make a tough decision:

1) Do they apply for a loan to survive the turbulent times

2) Or do they themselves start cutting their own spending (costs)?

They usually do both – take loans and cut their spending.

Taking this loan is often necessary, but risky.

They have to do it to survive, but paying back this loan is adding a long term expense, and taking away from the bottom line in the future.

What they do, is essentially gambling on better times to come before they run out of money again.

If it doesn’t, their even worse off than they were before they took the loan, because of the extra expense of paying it down with interest.

Other ways of cutting costs are to lay off employees.

This is also bad for the economy and of course terrible for the workers in the company.

When laying people off, the company produces less as well, which also leads to lower earnings.

The workers also earn less, and therefore start spending less, which causes other companies to earn less as well.

As you might see already, this is the start a downward cycle, in which low earnings lead to loans and lay-offs, which leads to higher costs and even lower earnings, which leads to more loans and lay-offs…

All this results in lower overall spending, and therefore earnings.

Step #2 to a financial crisis and inflation

After businesses struggle for some time, and a lot of people has lost their jobs, the collective spending of the nation’s people and businesses decrease even more.

This makes it even harder for businesses to survive.

At this point, regular people are struggling to pay their rents, as well as their mortgages.

Remember, when a person stops paying rent, the landlords earnings decreases, making it harder to pay of their mortgage, which is really bad.

After some time, a ton of people can’t pay their mortgages to the banks, and default their loans.

This leads to a huge loss of income for banks, and a ton of debt that never gets paid.

In addition, for the banks to give out new loans, they need a “reserve”:

This reserve needs to be 10% in most parts of the world. This means that if the bank has a reserve of one million dollars, they are allowed to lend out 10 million dollars.

In other words:

For every dollar you deposit to your savings account, the banks are allowed to loan out ten dollars.

When people stop paying their mortgages, this becomes a huge problem. The banks then have less money coming in, which restricts their loaning capability.

This makes it harder for businesses, and people to get loans. This leads to bankrupt businesses and people without jobs.

Credit is no longer available, as banks have low reserves, and the economy start feeling the withdrawal symptoms after being juiced up for years…

In summary, the decreased spending from regular people makes landlords unable to pay the banks, which again makes banks unable lend out money to struggling businesses – forcing them to cut costs (usually fire employees), decreasing the spending of regular people even more.

This cycle continues for a while, until step #3 kicks in:

Step #3 to a financial crisis and inflation

At this point the spending, as well as earnings, are low, both for people and businesses. In addition, banks can’t give out loans to temporarily keep businesses afloat, due to their decreasing reserves.

This means that the businesses that are struggling, and desperately need loans to survive the hardships, can’t get it.

Also, the credit that people acquired during “the good years” of the economy, makes this even worse.. People struggle to pay down their debt, and have to cut costs even more. This is the final straw that breaks the camels back…

This is what happens next:

Massive layoffs and bankruptcies.

The economy crashes.

The housing market plummets, as people are forced to sell their houses.

The stock market crashes, because of the economic crisis.

People’s pensions get drastically cut, because their funds were put into stocks and bonds, or real estate.

This really sucks, and it seems like there’s no way out of the hole. It’s a terrible situation to be in for the country, and for the people living in it.

How We (don’t) Deal With Financial Crisis

There are two alternative routes to take from this position:

1) Let it crash

2) Save it

Saving it seems like the obvious choice here, but it isn’t, really. Let’s compare the two alternatives, and look at the consequences:

1) Let the Economy Crash

Letting it crash would be awful in the short to mid-term. We’d go into a depression that probably would be worse than “the great depression”.

The long-term look is a lot brighter. After this horrible event, we would be on fertile ground.

The playing field would be evened out, there would be enormous potential for growth.

In the depression, we would most likely have experienced a deflationary period, the opposite of inflation.

The prices of everything would be lower, unfortunately, the earnings would also be lower, but we’d have more room to grow.

It sucks to live through deflation (opposite of inflation), but is good for the economy in the long term.

We would eventually start building ourselves up, creating a more sustainable economy. There would be less credit, and therefore more accurate earnings relative to production/productivity.

To recap, it would be terrible, horrifyingly terrible, in the short to mid-term, but over-all good in the long term.

2) Save the Economy

If we were to save ourselves from a depression, we’d have a much more pleasant short to mid-term, but a much worse long-term outlook.

We would skip the hole “terrible, horrifyingly terrible” period, and just artificially increase our earnings to the point where the economy would stay afloat.

We essentially have two weapons against a depression: Printing money and lowering the interest rates for loans.

Basically, what we do is inject cash into the economy, and incentivizing businesses to take more loans (credit). This leads to higher spending, and therefore higher earnings for others, which starts an economic recovery.

This would be great for the short-mid term, but it’s horrible for the long term…

How We “Save” the Economy (and why it’s bad)

The way this happens is that central banks start printing tons of money, and throws it at the economy. Specifically they start giving a ton of money to banks, the government and other big institutions.

They don’t give them money directly, but they buy stuff like “treasury bonds”, which basically is a government debt position from these institutions.

“Wait, what..?”

I know this sounds super complicated, but it’s not:

The way this all works, is that it starts with the government needing some money. Therefore, they create and sell “bonds”.

Creating a bond means creating credit for themselves. They lend themselves money, and promise to pay this back with interest.

This sounds stupid, I know. Why would they lend themselves money?

Well, what they do next makes it more logical:

They call the new loan they gave themselves “a bond”, and sell it to investors.

The amount that the investors pay the government for the bond, is the amount of money that the government “lend” to themselves.

The government then has the new money. They pay the investors interest for owning the bond/debt.

Still a little unclear?

Let’s go through how this process works, step-by-step in detail:

How Central Banks Create New Money:

The government creates a bond to raise some money, let’s say one million bucks.

Then, someone buys this bond from the government, effectively giving the government one million bucks.

The government now has one million dollars, and the guy that bought this bond now owns the bond, which is valuated at one million dollars.

He can either hold on to this bond, or sell it to someone else.

The incentive he has to hold it, is that he receives a “yield” on this bond. The government basically promises to pay him interest, usually around 2-8 % per year.

In this example, with a yield of 5%, the guy buying the bond would now have the bond worth one million dollars, and receive $50 000 (5% of one million) every year he holds it.

The interesting part is that there was only one million dollars of value to begin with, but now the government has one million dollars to spend, and the guy has one million dollars’ worth of bonds.

Essentially, there’s been created one million dollars. This million is in the form of debt, so new money hasn’t been created, but the government now has new “money” to spend.

The way that the Federal Reserve (Central bank of the US, also known as the FEDs) injects new money into the economy, is by buying up these bonds from different institutions.

This way, they remove the newly created debt, however, the investor and the government still keep their one million bucks.

In other words: The Federal Reserve pays off the debt that the government has to the investor.

However, they don’t by bonds from average investors like you and me. The list is limited to banks and other major institutions. Let’s look at what happens from start to finish, to really understand how this all works:

Practical Example of Injecting $50 million Into the Economy:

The Government needs some money. Therefore, they issue a bond worth 50 million dollars with a yield of 3%.

A bank, looking for a new investment, buys it, and start receiving a nice yield of 1,5 million dollars every year.

The government now has 50 million to spend, and the bank owns 50 million dollars’ worth of government bonds.

This is where the FEDs comes in:

They decide it’s time to juice up the economy with 50 million freshly minted Benjamin’s.

They then go on to buy the bonds that the bank owns.

The bank now has 50 million dollars from selling the bond to the FEDs, the government has 50 million dollars to spend, and the FED sits on the bond worth 50 million dollars.

They have effectively pushed 50 million dollars into the economy, and taken the bond out of it.

The government still has increased their spending power with $50 million, the bank now has more cash, and the feds sit on this bond.

“Sure, but how does this help the economy?”

Both the government and the bank now have the potential to spend 50 million dollars, and as you already know, this means higher earnings for someone else.

In other words, to inject cash into the economy the FEDs buy bonds from banks and other major institutions. These institutions now spend more money, which means other institutions start earning more money. These institutions can also start spending more, which then kicks off a positive spiral upwards.

Another positive effect of this is that the banks, when they receive cash, are able to give out more loans:

Remember, they need to keep a certain percentage in reserves, and when they receive new money, this replenishes these reserves.

They’re now able to inject steroids (credit) into the economy, which leads to an accelerated recovery due to higher spending.

This is, simplified of course, how the Federal Reserve is able to save the economy by injecting cash into it – buying bonds from large institutions.

Below you see the “M2 Money Stock”, going back to 1981:

This metric measures the number of dollars available in the economy, the supply of USD. If the supply increases, it means that central banks have printed money, or new debt has been created.

Notice the “spike” we had recently? Well, that’s our response to COVID-19.

Even my Grandmother could recognize that this chart is trending upwards at an exponential rate.

This exponential growth is not going to slow down, as The Federal Reserve has no plans of increasing the interest rates, and do plan on continuing buying bonds (printing money).

(Source: https://www.marketwatch.com/story/fed-sees-rates-near-zero-through-2022-says-asset-purchases-will-continue-2020-06-10)

Money-printing, combined with low interest rates, is a good defense against potential depressions, as it produces more spending and therefore economic expansion and growth.

However, there’s no such thing as a free lunch…

There are consequences to printing money and lowering interest rates…

The Consequences of Inflation – Inequality

Free money and low interest rates sound like a great economy, right? Why do we even bother paying our taxes, when they could just as easily print the equivalent amount for free? Heck, why even go to work when money can be printed?

Even though these questions sound ridiculous, they’re legit questions. A lot of people ask questions like these when they learn about the money printing.

There are two answers to those questions:

1) If we all stopped working, the economy would stop.

We need to work. We need to produce. At least until we can replace our workers, and automate functions with robots and AI software.

2) Printing money isn’t actually crating more value, but only hurts the economy in the long run.

This is easiest to explain with a kind of silly, but effective analogy:

Imagine the economy as a pizza. Every asset in the world makes up this pizza. Let’s say you own a small portion of this. You own ten thousand dollars worth of stocks, and therefore own a ten thousand dollars big slice of the economy-pizza.

When the FED injects cash into the economy, one would think that the pizza grew, and got larger, but that’s wrong.

For the pizza to grow, the asset itself has to grow. When we produce something, the pizza gets larger. When we make new stuff, or make old stuff better, the size of the pizza increases.

When the FED injects cash into the pizza, they change how large the slices are, not the size of the actual pizza.

This is really bad news for people trying to acquire pizza slices, or people who has their money in savings. This hurts the poor and middle class, and increases the divide between the rich and the poor…

Why inflation hurts the poor and middle class

Let’s say the economy-pizza has one million slices before injecting cash. After injecting cash, we all of a sudden have 1,1 million slices, without the pizza getting bigger.

Every pizza-lover knows that more slices equal smaller slices. It’s impossible to maintain the slice-size when increasing the number of slices.

The same thing happens when injecting cash into the economy:

The 10 000$ slice you own has gotten smaller.

It’s still worth 10 000$, but the actual value of your slice, the size of it, is now smaller than it was before the cash injection.

Now ask yourself, if the slice has gotten smaller, but it’s still worth 10 000$, is the dollar still worth the same amount as it was before the injection?

The answer is no.

The dollar loses value every single time the FED injects cash into the economy.

The amount of dollars needed to acquire a given slice of the economy-pizza increases. The purchasing power of the dollar decreases.

This is a bad thing for people who don’t have, or only have small slices, as it gets harder and harder to acquire more, and the slices that one owns get smaller and smaller.

The only solution is to have your money invested in something that can outrun the “rate of inflation”.

The rate of inflation, is the rate at which your money loses their value, or the rate at which the slices you can afford for a given amount of dollars decreases.

Inflation is good for economic stimulation, to kick the economy back up when it starts slowing down, but it’s bad for people trying to acquire slices of the pizza, or for people who have their money in savings/cash.

In 2020, the M2 money supply was increased by 25%. This means that we have cut the economy-pizza into 25% more slices, and decreasing the size of the existing slices with 25%. This is bad, really bad…

Bitcoin – Hedge Against Inflation

As mentioned, the only way to save yourself from the inevitable value-decrease caused by inflation, is to have you capital invested in something that outruns the rate of inflation.

Bitcoin is the best candidate for this. Bitcoin is designed to be an asset which holds your value intact – a store of value.

Due to it’s unique attributes, it is the best place, in my opinion, to park your money when trying to escape inflation.

Why, you ask? Because of three things:

1) It’s Decentralized

This means that no central authority can alter it. The Federal Reserve controls the Dollar supply, which is why they can print as much as they want.

This will never happen to Bitcoin, as no one controls it’s supply. Everything is pre-programmed, and (basically) unchangeable.

2) The Halving

The halving refers the the event happening every four years, where the inflation rate of Bitcoin is cut in half.

To be more specific, the rewards that miners receive for validating transactions are halved. This might sound trivial, but it’s actually the backbone of bitcoins value.

This basically cuts the inflation rate of new Bitcoin in half every four years.

3) Absolute Scarcity

There is a maximum supply of Bitcoin, capped at 21 million. This means that there will never be more than 21 million Bitcoin in circulation.

This makes Bitcoin an “absolute scarse” asset, which is a necessary quality for a good store of value. This is the main reason gold has been so effective at storing value – it’s hard to make more of it.

Among other qualities, these two make Bitcoin a perfect hedge against inflation, and the best “store of value” there has ever been.

Suggested reading:

Read more about the Halving, and what gives Bitcoin value

Read about how Bitcoin will take over the role as Global Reserve Currency and knock out the United States Dollar

The Inverse Relationship Between USD and BTC

Bitcoin and the Dollar have an inverse relationship. This means that they move in opposite directions.

This is because if the dollar loses strength, the faith in the FIAT (traditional currencies like USD, EURO, YUAN) currencies weaken, and the demand for Bitcoin increases.

People are using Bitcoin as a hedge against the weakening of the U.S Dollar.

The graph below shows the DXY (U.S. Dollar Index). I have marked the general trends, and what Bitcoin did within those same times. Notice how they do the exact opposite of each other.

It’s clear as day that the U.S Dollar and Bitcoin have an inverse relationship. In the legendary 2017 bull-run of Bitcoin, the Dollar had a bear market, going down significantly. Basically the same week as Bitcoin started crashing, the first week of 2018, the U.S Dollar start it’s bull run.

The current bull market in crypto is also accompanied with a bear market for the U.S Dollar, further cementing the inverse relationship between the two giants.

Bitcoin Replacing Gold as a Hedge Against Inflation

Before Bitcoin, investors turned to gold in times of uncertainty. The trend we’re seeing now, is that instead of using gold as a hedge against inflation, investors are using Bitcoin as their new inflation-defense.

According to JP Morgan, institutions are increasingly choosing Bitcoin over gold when inflation looms. (Source: https://news.bitcoin.com/jpmorgan-gold-etfs-bitcoin/)

This is what companies like Tesla and Micro Strategy has done. They don’t invest billions of dollars into Bitcoin to make money, they do it not to lose money.

This might be the beginning of the end for both gold and the dollar, as Bitcoin is hijacking market share from both of them.

I created an infographic that shows you the market capitalization (total value of all BTC/USD/Gold) of the three. I think it’s safe to say that Bitcoin has plenty of room to grow:

Do You Invest in Bitcoin?

This Bitcoin bull market will be remembered. We have institutional acceptance, and adoption, at levels no one saw coming.

Make sure that you take full advantage of this opportunity. Make sure that you maximize your ROI in all ways you can.

Download my free guide on how to maximize returns, and sign up to my newsletter. I’ll provide market updates, and technical analysis on altcoins and Bitcoin on a regular basis.

If you want to help me reach more people, please share this post on social media!